Hapag-Lloyd’s annual report for 2023 and financial results for Q4 reveal exactly how difficult the ocean container market has been for the biggest steamship lines. The report, which the German container ship line released Thursday, notes that Liner Shipping revenues dropped 48.5% to 17.7 billion euros ($19.2 billion) from 2022 to 2023, and earnings before interest, taxes, depreciation and amortization fell by 77.1% to 4.4 billion euros over the identical period.

The ocean carrier grew its volumes barely, from 11.8 million twenty-foot equivalent units to 11.9 million TEUs, however the collapse of average freight rates from $2,863 per TEU to $1,500 per TEU meant that Hapag-Lloyd took in much less money for each box it moved, crushing its margins and profitability. As a bunch — in other words, consolidated Liner Shipping and Terminal and Infrastructure results — Hapag-Lloyd managed to generate profits of two.9 billion euros in 2023, down 82.6% from 17 billion euros in 2022.

Note that Hapag-Lloyd’s 2023 results were still the third-best profitability lead to the group’s history; the steep decline in freight rates, revenues and EBITDA indicated the popping of the pandemic-era bubble in transportation demand slightly than any fundamental weakness in Hapag-Lloyd’s business.

But when it got here time to debate Hapag-Lloyd’s financial results on CNBC, CEO Rolf Habben Jansen was already painting a rosier picture: Inventories are depleted worldwide, Habben Jansen said, and the volumes were picking up nicely after the Lunar Recent Yr. Peak season will come early this 12 months, he predicted.

“I might also expect that peak season goes to start out a little bit bit early,” Habben Jansen told CNBC. “I also expect that there’ll be quite a variety of individuals who tried to usher in their goods somewhere between June and August.”

Typically, ocean container peak season runs from September to October, effectively ending with Golden Week annually. That provides importers enough time to choose up boxes on the port, transload them at nearby warehouses, after which move them to inland distribution centers by rail or truck, ingesting them into their domestic supply chain in time for peak retail season in November and December.

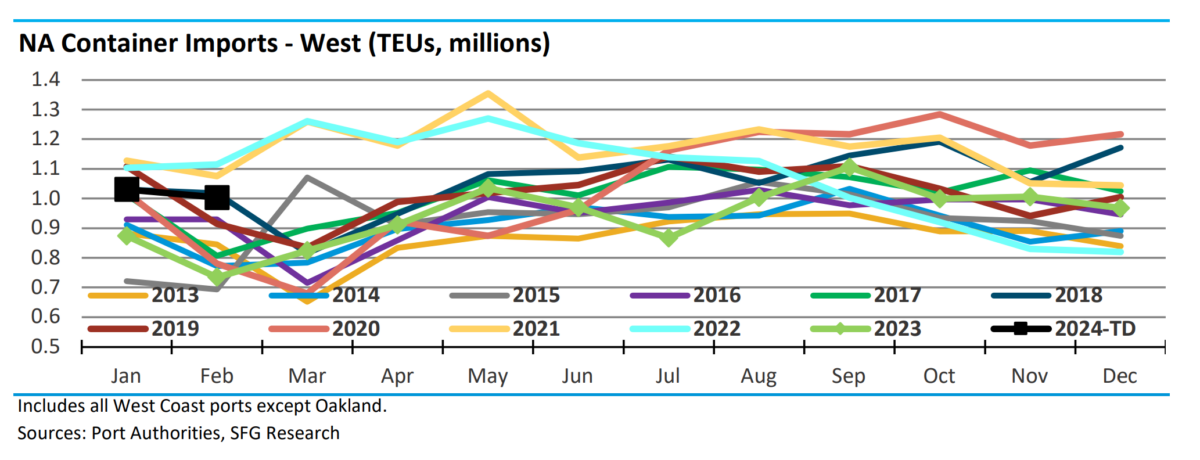

To this point, 2023 containerized imports have began off strong, but favorable year-over-year comps have also been supported by the timing of the Lunar Recent Yr. In 2023, the vacation began on Jan. 22, while it began on Feb. 10 this 12 months. The historical imports data within the chart above shows that the depressed volume effects following the vacation are roughly evenly split between February and March, depending on the 12 months — 2024 should see a weaker March.

If Habben Jansen is correct, though, soft conditions won’t last long, and we might even see elevated, peak-ish volumes as soon as early summer. The pondering here is that while labor conditions at West Coast ports have stabilized since last 12 months’s contract negotiations, it’s now the East and Gulf Coast ports’ time to settle up with their unions. Strikes are all the time on the table as dockworkers attempt to put pressure on port authorities prior to the signing of those vital multiyear agreements, so shippers, Habben Jansen believes, will try to maneuver their goods into the country earlier slightly than later.

The post Hapag-Lloyd CEO predicts early peak season for ocean shipping appeared first on FreightWaves.

{kind=link}