Chart of the Week: Producer Price Index – all commodities, Consumer Price Index – all, Outbound Tender Volume Index – USA SONAR: PPI.ALLCOM, CPI.ALL, OTVI.USA

The Producer Price Index (PPI), which measures the input costs for goods, has fallen 8% since last summer. The Consumer Price Index (CPI), which measures what consumers pay for goods and services, has kept increasing. Corporations are still attempting to get their margins back to pre-pandemic levels with price increases on finished goods. It will proceed to place freight demand in danger within the second half of the 12 months.

The PPI does have a transportation cost component to it, so it just isn’t surprising that after truckload freight demand — measured by the Outbound Tender Volume Index (OTVI) — collapsed in March of 2022 the PPI began to say no just a few months later. That is representative of the start of supply chains becoming less congested and the flow of products flowing more freely.

One reason for the still rising CPI figures — what the Fed uses as a measure for inflation — is a lagging response by corporations to pass along the increasing input costs within the early phases of the pandemic.

The PPI increased 20% throughout 2021, while the CPI only rose 6.7%. It’s typical for corporations to carry off on price increases and take a look at to soak up as much of the price as possible on the front end in order to not shock their customers into in search of replacements. That is why inflation is such a lagging indicator.

Goods demand has been eroding since 2021, something corporations had trouble recognizing as a result of their difficulties sourcing materials. They were never in a position to count on receiving enough inventory.

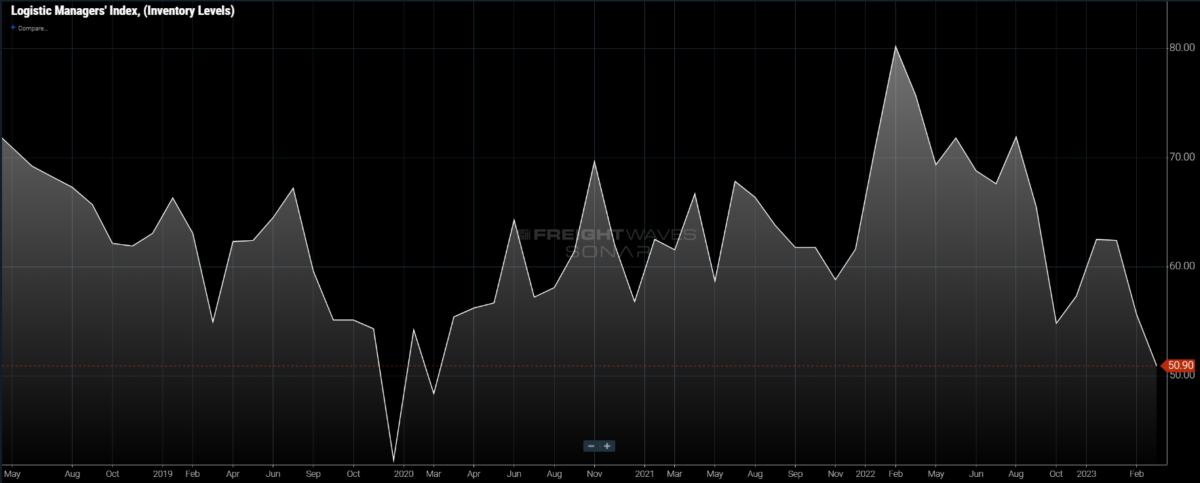

Inventory levels are getting closer to being in step with company targets as indicated by the recent Logistics Managers’ Index (LMI) report that shows a reading of the bottom level of expansion since March of 2020. As inventories normalize, discounts change into less likely and price increases on base goods proceed. This puts future demand within the hands of the consumers, who’re being put under continuous pressure to spend less.

How much can consumers take?

Consumers received windfalls of money through the pandemic in the shape of stimulus packages and prolonged unemployment advantages. Additionally they had way more free time, which led to the patron spending bubble.

The issue now could be that the bubble has burst and consumers have yet to feel the complete effects of continuous Fed rate increases and declining purchasing power. The roles market can be showing cracks with jobless claims on a consistent rise to begin the 12 months.

Wage growth has not been in a position to sustain with inflation at many levels. The service sector, which had a boom in 2022 after lockdowns led to the U.S., is now beginning to see the consequences of diminishing consumption.

The fact is that corporations are actually driving many of the inflation as they get better margins, not the patron.

It’s not all doom and gloom

There may be optimism left, nevertheless. Zac Rogers, a contributor to the LMI, talked on this past week’s Freightonomics about how upstream participants in supply chains are more optimistic about demand later within the 12 months as they expect the Fed to take a pause on rate hikes. It will open the door for a more stable investment environment. He states it’s less concerning the rate and more concerning the expectation.

Downstream participants are usually not as optimistic, but additionally they are inclined to feel things on a lag in comparison with upstream. Unfortunately for a lot of transportation providers, this also may mean probably the most overserved sectors that grew on the backs of consumption won’t feel the economic recovery till later.

In regards to the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from hundreds of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, continue to exist the front page. After that, the Chart of the Week will probably be archived on FreightWaves.com for future reference.

SONAR aggregates data from tons of of sources, presenting the info in charts and maps and providing commentary on what freight market experts need to know concerning the industry in real time.

The FreightWaves data science and product teams are releasing latest datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Way forward for Supply Chain

JUNE 21-22, 2023 • CLEVELAND, OH • IN-PERSON EVENT

The best minds within the transportation, logistics and provide chain industries will share insights, predict future trends and showcase emerging technology the FreightWaves way–with engaging discussions, rapid-fire demos, interactive sponsor kiosks and more.

{kind=link}