This week’s FreightWaves Supply Chain Pricing Power Index: 35 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 40 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 40 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to research the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is predicated on the next indicators:

A break within the clouds

After an eventful January during which carriers benefitted from unseasonal tightness brought on by severe winter storms, I argued that freight markets were showing signs of a long-lasting recovery. I took pains to make clear that this recovery was not going to be a roller coaster of unstoppable growth, that it was as an alternative a gradual rebalancing of market dynamics. Even with that caveat, the recent performance of tender rejections and spot rates has been more disappointing than I expected — as will likely be discussed below.

But before moving onto the doom and gloom, I need to restate my bull case for the approaching months. At the same time as carriers’ pricing power deteriorated, freight demand was consistently robust throughout February. Looking forward to the months ahead, there remains to be significant room for growth as Chinese imports hit the West Coast in the approaching weeks. The early stages of produce season are forecast to see yearly growth in Texas and Florida, helped partially by El Niño’s weather patterns. Activity in the development sector will likely be aided by federal funds allocated to manufacturing, transportation infrastructure and energy infrastructure, while homebuilders project a fair higher 12 months ahead than the already-busy 2023.

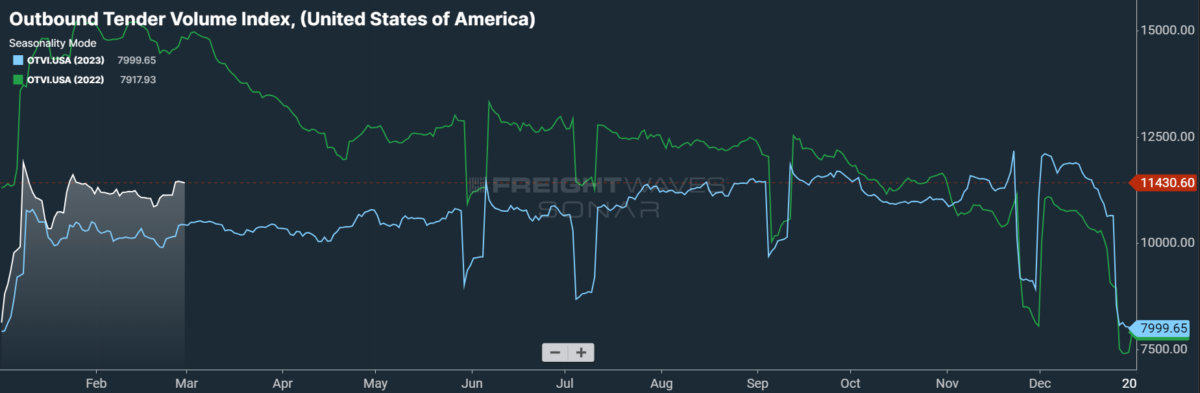

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ requests for capability, is up 3.38% week over week (w/w). On a year-over-year (y/y) basis, OTVI is up 11.71%, though such y/y comparisons may be coloured by significant shifts in tender rejections. OTVI, which incorporates each accepted and rejected tenders, may be inflated by an uptick within the Outbound Tender Reject Index (OTRI).

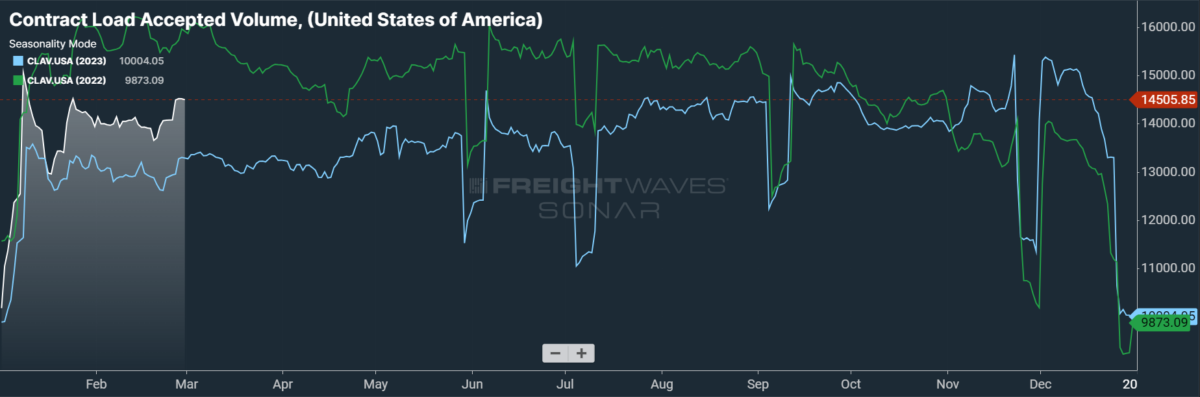

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In brief, it is comparable to OTVI but without the rejected tenders. accepted tender volumes, we see an increase of 4.09% w/w in addition to one in all 9.15% y/y. This positive y/y difference implies that actual freight flow is recovering from this cycle’s bottom.

As stated above, there are numerous reasons to be hopeful in regards to the near-term way forward for truckload demand. Freight activity was sustained in late January and February by high import volumes. The Port of Latest York and Latest Jersey recently reported that January 2024 was the third-busiest begin to the 12 months on record, lagging behind only the incredible growth of 2021 and ’22. Meanwhile, on the alternative coast, the Port of Los Angeles — the busiest port within the U.S. — saw its second-best January this 12 months, surpassed only by 2022.

Couple this growth with the undeniable fact that import bookings from China to the U.S. set record highs in the primary two weeks of February (that’s, within the run as much as Lunar Latest 12 months) and that these bookings were made roughly 42 days before the shipments arrive on U.S. shores, late March and early April ought to be incredible months for truckload markets near West Coast ports.

There are other positive signs for activity beyond maritime volumes, nonetheless. Bank of America’s Truckload Demand Indicator for shippers hit its second-highest level in 80 weeks at the top of February, up 13% y/y. This particular index surveys demand over the following three months, though shippers are much more bullish over the following six to 12 months. That said, most of the shippers surveyed note that they’ve yet to see “the exodus of trucking firms” normally witnessed at this point within the cycle, with excess capability remaining a headwind towards rebalancing the market.

Finally, flatbed demand particularly ought to be buoyed by growth in construction and manufacturing. The S&P Global US Manufacturing PMI saw its headline index rise from 50.7 in January to 52.2 in February, indicating more rapid expansion. S&P Global stated that manufacturers saw the steepest growth in recent orders since May 2022, with demand rising from customers each foreign and domestic. “After an extended spell of reducing inventories to chop costs,” wrote Chris Williamson, chief business economist at S&P Global Market Intelligence, “factories at the moment are increasingly rebuilding warehouse stock levels, driving up demand for inputs and pushing production higher at a pace not seen since early 2022.”

Meanwhile, homebuilders are notably optimistic about their lots in 2024. Economists speaking on the National Association of Home Builders’ recent International Builders’ Show stated consensus expectations of 5% y/y growth in single-family housing starts, forecasting two or three Federal Reserve rate cuts of 25 basis points each within the latter half of the 12 months. Bank of America evaluation is much more bullish, expecting a 20% y/y rise in single-family starts over the primary quarter and a 9% y/y gain for 2024 in total.

Where have all of the truckers gone?

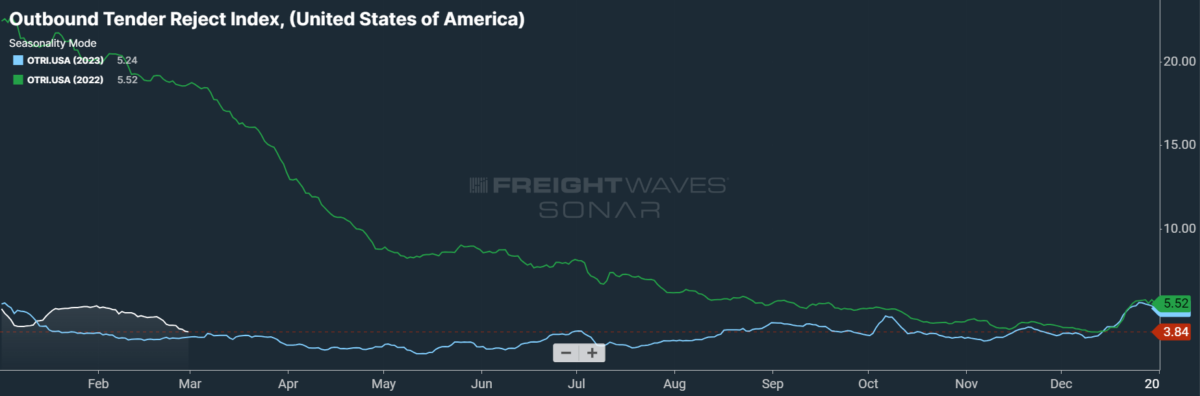

There are good reasons to feel hopeful in regards to the way forward for freight demand in 2024, however the Pricing Power Index didn’t fall to 35 this week without cause. After treading above 5% for much of January and a few of February, OTRI has since depreciated to sub-4% levels. While these movements are relatively minor on the grand scale of things, the direction is vital here. A rising OTRI may be an inflationary force to identify rates if it tracks above 7% — give or take — or if it makes rapid gains over a brief time period. But while OTRI was indicative of capability trickling out of the market, it isn’t any longer.

Perhaps the strangest thing about capability on this cycle is the way it differs from the info. Many economists have noted the apparent discrepancy between government data on the labor market, which is incredibly strong, and the various reports of mass layoffs reaching a lot of industries.

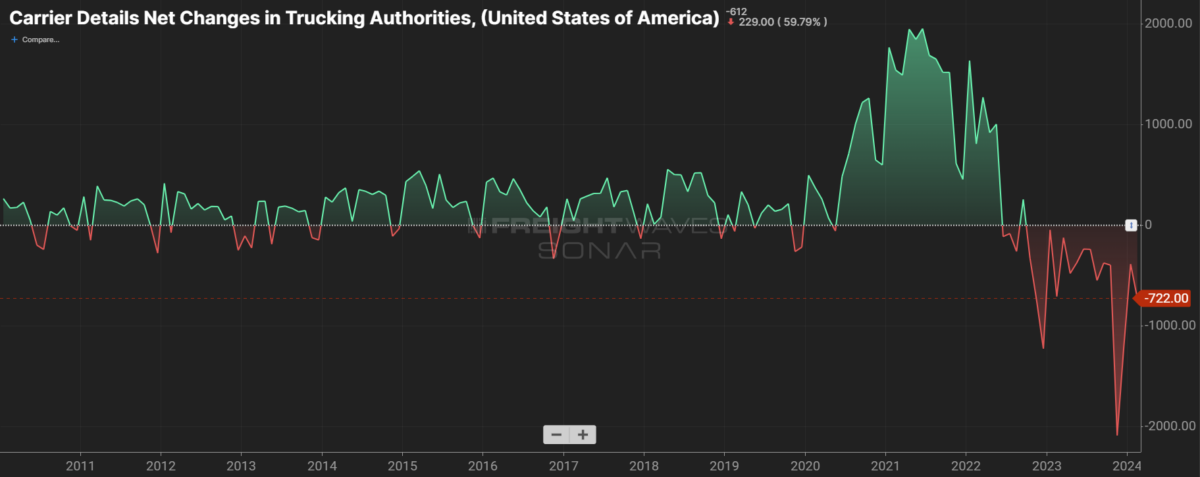

Yet the trucking industry not only has its justifiable share of newsworthy layoffs and bankruptcies, it also has the info tracking carriers leaving the market. Federal Motor Carrier Safety Administration data on the web changes of carrier authorities (below) shows that a greater variety of carriers have left the industry than have entered in every month since October 2022 — despite the undeniable fact that many owner-operators are inclined to let their authorities quietly expire relatively than trouble with official revocation.

The web losses of authorities should not insignificant, either: Before the present cycle, the month during which the most important variety of carriers left the industry without alternative was November 2016, which saw a net lack of 329 authorities. Greater than six times that number vanished in November 2023, which posted a net lack of 2,087 authorities.

As stated previously, this data doesn’t even capture the complete scope of the capability runoff happening. FMCSA requirements state that interstate carriers must renew their authorities every two years. Because it just isn’t unusual for carriers to exit the industry only temporarily — that’s, only until the following upturn occurs — a lot of those leaving don’t trouble with official revocation. As a substitute, they either renew their authorities if the industry is booming or else let it expire quietly. This behavior implies a lag of as much as two years for the FMCSA to effectively measure the quantity of capability runoff.

The longest shortest month

February was simply abysmal for small carriers primarily exposed to the spot market. Over the course of the month, fuel-inclusive spot rates fell by a national average of 21 cents per mile. Most of the nation’s largest carriers have also weighed in on 2024’s bid season for contract rates: Werner Enterprises, with understatement characteristic of corporate businesses, said that this 12 months’s round of contract negotiations was “very competitive.” That said, some shippers have stated that their recent rates won’t go into effect until as late as April, while other contract rates are indexed to data from the broader economy — akin to the inflation-tracking Consumer Price Index — and so are less vulnerable to market dynamics of the trucking industry.

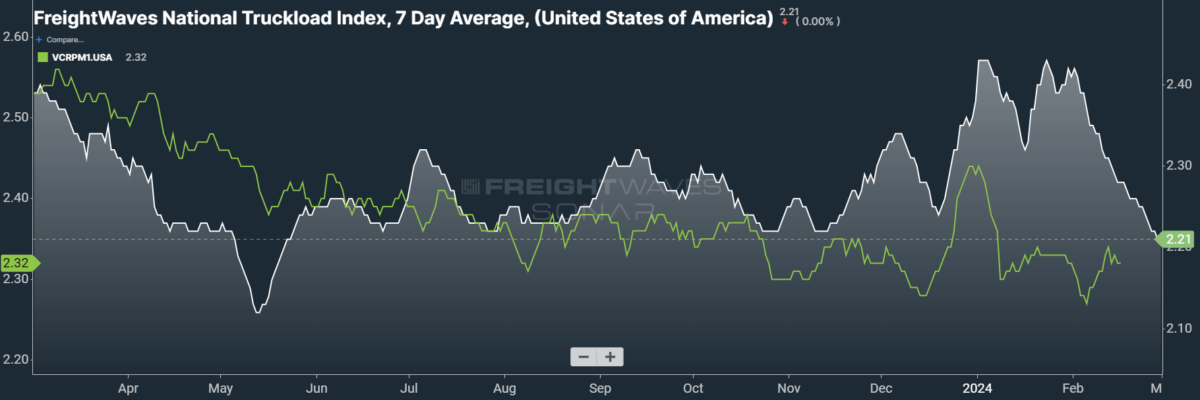

This week, the National Truckload Index (NTI) — which incorporates fuel surcharges and other accessorials — fell 4 cents per mile to $2.21. Sliding linehaul rates were wholly answerable for this week’s loss, because the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — fell 4 cents per mile to $1.58.

Contract rates, that are reported on a two-week delay, have recovered somewhat from a dip in early February. Nevertheless, they’re tracking near 2021 levels from before the speed bonanza of this current cycle. By the beginning of Q2, there will likely be a more definite answer as to how this bid season impacted carriers. In the intervening time, contract rates — which exclude fuel surcharges and other accessorials just like the NTIL — are unchanged on a weekly basis at $2.33 per mile.

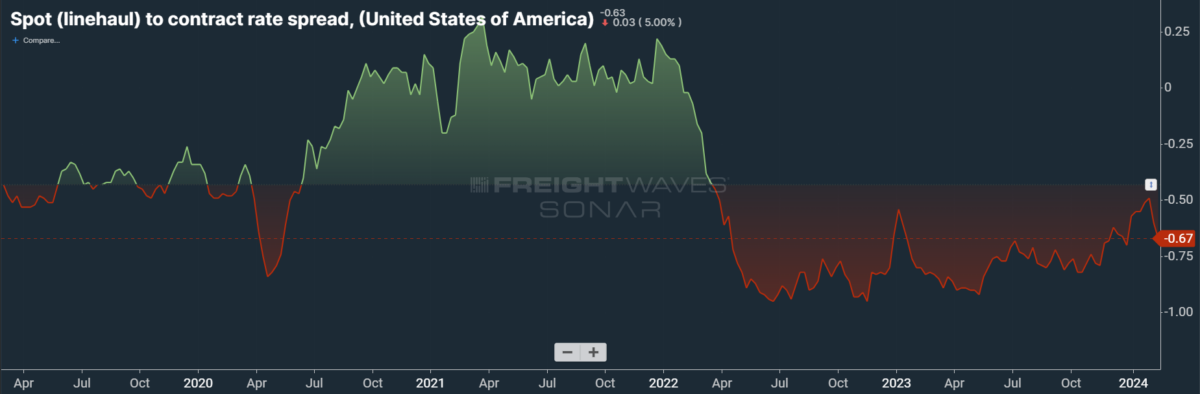

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the info set, which dates to early 2019. Throughout that 12 months, contract rates exceeded spot rates, resulting in a record variety of bankruptcies within the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs seemingly weekly, while contract rates slowly crept higher throughout 2021.

Over the course of 2023, this spread averaged 10 cents lower than in 2022, indicating that contract rates had yet to return into balance with the market’s fundamentals of carriers’ supply and shippers’ demand. These lopsided fundamentals were more appropriately reflected in spot rates, that are highly reactive to shifting market conditions. As linehaul spot rates remain 67 cents below contract rates, marked signs of rebalancing are starting to look, though there remains to be room for contract rates to say no — or for spot rates to rise — in the primary half of 2024.

For more information on FreightWaves Research, please contact Michael Rudolph at mrudolph@freightwaves.com or Tony Mulvey at tmulvey@freightwaves.com.

The post Beware the false spring appeared first on FreightWaves.

{kind=link}