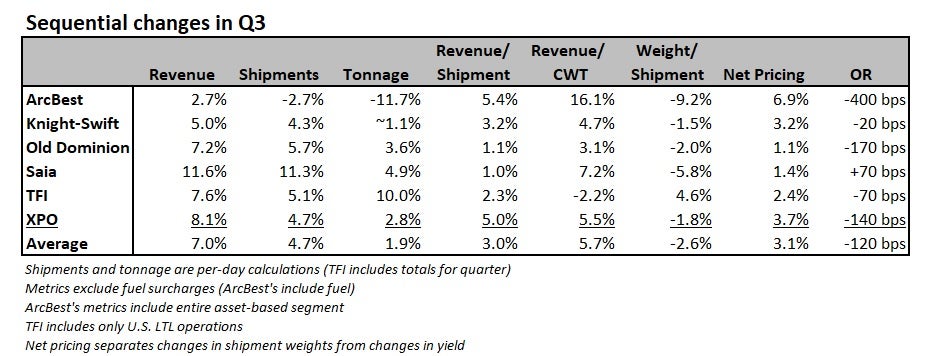

The third-quarter earnings season showed all publicly traded less-than-truckload carriers experienced some kind of bump following Yellow’s exit. If it was a contest, Saia was the winner.

While there’s just a little noise within the numbers, the sequential progression from the second to the third quarters is a very good yardstick of how Yellow’s $5 billion freight share was redistributed. Yellow had been teetering for years but as tensions rose with its union workforce within the June-July time-frame, shippers and 3PLs began moving their freight with other carriers. The third quarter could have not captured everything of the event but it surely is an awesome representation of what happened.

Also value noting, private regional carriers and top 5 national operator Estes were likely market share takers within the period, however the market isn’t aware about their results.

Saia (NASDAQ: SAIA) reported an 11.3% increase in shipments per day from the second to the third quarters. The carrier added greater than 1,000 employees within the period, constructing on an existing head count of roughly 12,000, to accommodate the influx.

The tighter capability backdrop pushed yields higher.

Its revenue per hundredweight increased 7.2% excluding fuel surcharges. The calculation was bolstered by lower shipment weights, an occurrence seen throughout the industry because the broader industrial and manufacturing complexes have cooled. When accounting for the lighter weights, yield was likely up just modestly on a sequential basis.

The corporate’s operating ratio — operating expenses expressed as a percentage of revenue (the lower the higher) — deteriorated 70 basis points sequentially within the quarter to 83.4%. Nevertheless, the backslide was modest given the prices it incurred to tackle the freight windfall. The quarter also contended with a July wage increase averaging 4.1%.

“SAIA is capitalizing on a once in a generation market share opportunity within the LTL market,” Deutsche Bank (NYSE: DB) analyst Amit Mehrotra said in a Friday note to clients. “This comes with extra costs on the front end, but customers are prone to stay and pay more over time.”

5% is the figure for many

Most carriers saw a 5% sequential increase in shipments in the course of the quarter.

Old Dominion’s (NASDAQ: ODFL) “investing ahead of the curve” strategy allowed it to post a 5.7% increase in every day shipments with minimal disruption to service. The corporate has grown door capability roughly 50% through $2 billion of real estate investments over the past 10 years. It typically operates its network with 25% latent capability, allowing it to take market share while maintaining service commitments to existing customers.

The corporate recently earned best-in-class honors amongst national carriers for a 14th straight yr, in accordance with an annual shipper survey conducted from June to October.

Higher yields and price management at Old Dominion led to a 170-bp sequential OR improvement within the period.

The corporate doesn’t think the freight reshuffle is totally settled either.

“We’re hearing about competitors which can be missing pickups,” Old Dominion CFO Adam Satterfield said on a Wednesday call with analysts. “They don’t have the people a part of the capability equation solved and possibly took on an excessive amount of freight and are beginning to have negative implications from their overall service product.”

The comments align with a recent Morgan Stanley (NYSE: MS) survey of shippers and 3PLs that previously used Yellow. Thirty-five percent of those polled said that while they’ve already placed their freight with a brand new carrier, they’ll still be seeking to make a change in the approaching months.

XPO (NYSE: XPO) said per-day shipment counts increased by greater than 1,000 in every month of the third quarter to greater than 54,000 per day in September. All in, every day shipments were up 5% from the second to the third quarters and yields moved 6% higher excluding fuel surcharges.

The corporate used internal cost initiatives and favorable pricing trends to record 140 bps of sequential OR improvement, which was 370 bps higher than its historical seasonal trend. Contractual agreements renewed 9% higher within the period, which was nearly twice the extent recorded within the second quarter.

Shares of XPO were up 15% on Monday following the better-than-expected report.

XPO said it could also speed up growth in its network in response to tightening capability throughout the industry. A two-year plan will add 900 latest doors to its coverage map by the primary quarter of next yr.

TFI International’s (NYSE: TFII) U.S. LTL segment (TForce) recorded a 5.1% sequential increase in shipments. The share was just a little higher at the height of the disruption but TFI has seen some slippage of that captured freight in recent weeks. The share gains are coming at a time when TFI continues to be engaged in an initiative to purge low-margin business from its network.

The segment’s yields were down 2.2% sequentially excluding fuel surcharges but that metric was negatively impacted by a 4.6% increase in weight per shipment. Actual pricing was likely 2.4% higher sequentially. The OR improved 70 bps even with a higher-cost labor contract taking effect Aug. 1.

Knight-Swift Transportation’s (NYSE: KNX) LTL unit recorded a 4.3% increase in shipments from the second to 3rd quarters. Excluding fuel surcharges, yield improved 4.7% but a 1.5% decline in average shipment weight was a tailwind.

ArcBest’s (NASDAQ: ARCB) shares jumped 16% on its third-quarter report.

The corporate’s asset-based segment, which incorporates LTL carrier ABF Freight, saw shipments decline 2.7% from the second quarter. Nevertheless, the change is just a little misleading because it had been using dynamic pricing tools, which higher match available capability within the network to transactional shipments available in the market, to maintain loads elevated through the downturn.

The corporate began moving capability from transactional customers to cover shipment needs at accounts under contract. Those accounts were diverting freight from Yellow throughout July because it became evident the carrier would fail. When comping ArcBest’s July exit rate to the masses its targeting currently, shipment counts are up roughly 5%. Nevertheless, amongst its core accounts, shipments have increased greater than 20% since Yellow’s closure.

The segment’s OR improved 400 bps sequentially despite the fact that a brand new labor contract was a 350-bp headwind within the period.

“We’re really targeting a freight profile that maximizes the profitability in our network,” CFO Matt Beasley told FreightWaves.

Will favorable capability dynamics diminish when Yellow’s terminals reopen?

Bids on the 170-plus terminals Yellow owns are due Nov. 9. In September, a Delaware bankruptcy court approved an order naming Estes’ $1.525 billion stalking horse bid the winner. The agreement sets a base bid for Yellow’s owned terminals. Estes is unlikely to purchase the entire properties but it surely could walk away with a few dozen.

Those properties, in addition to the 100-plus terminals Yellow leased, may very well be back in motion in the approaching months. The brand new owners will likely wish to ramp throughput on the sites earlier than later to start out generating returns on those assets. But that doesn’t mean LTL rate cuts are likely.

“We’ve been in a freight slump here, in order that’s why we had capability as a bunch to fill within the holes for purchasers. But for those who get back to a more normalized industrial environment, we get some growth going again, you get port activity going again, you get advantages of nearshoring, well then that’s one other moat around pricing,” said Saia’s CFO Doug Col on a Friday conference call.

Also, a few of the sites will likely be acquired by strategic investors and repurposed to other sectors.

“There’s going to be some cases that a few of those don’t get returned to the LTL business because possibly the economics make more sense for that to show right into a warehouse or industrial real estate property of some kind,” said Fritz Holzgrefe, Saia’s president and CEO.

- ArcBest prudent in approach to latest freight opportunities

- Auction houses to liquidate Yellow’s tractors, trailers

- Heartland books Q3 loss, cuts unprofitable customers and lanes

The post Where did Yellow’s freight go? appeared first on FreightWaves.

{kind=link}