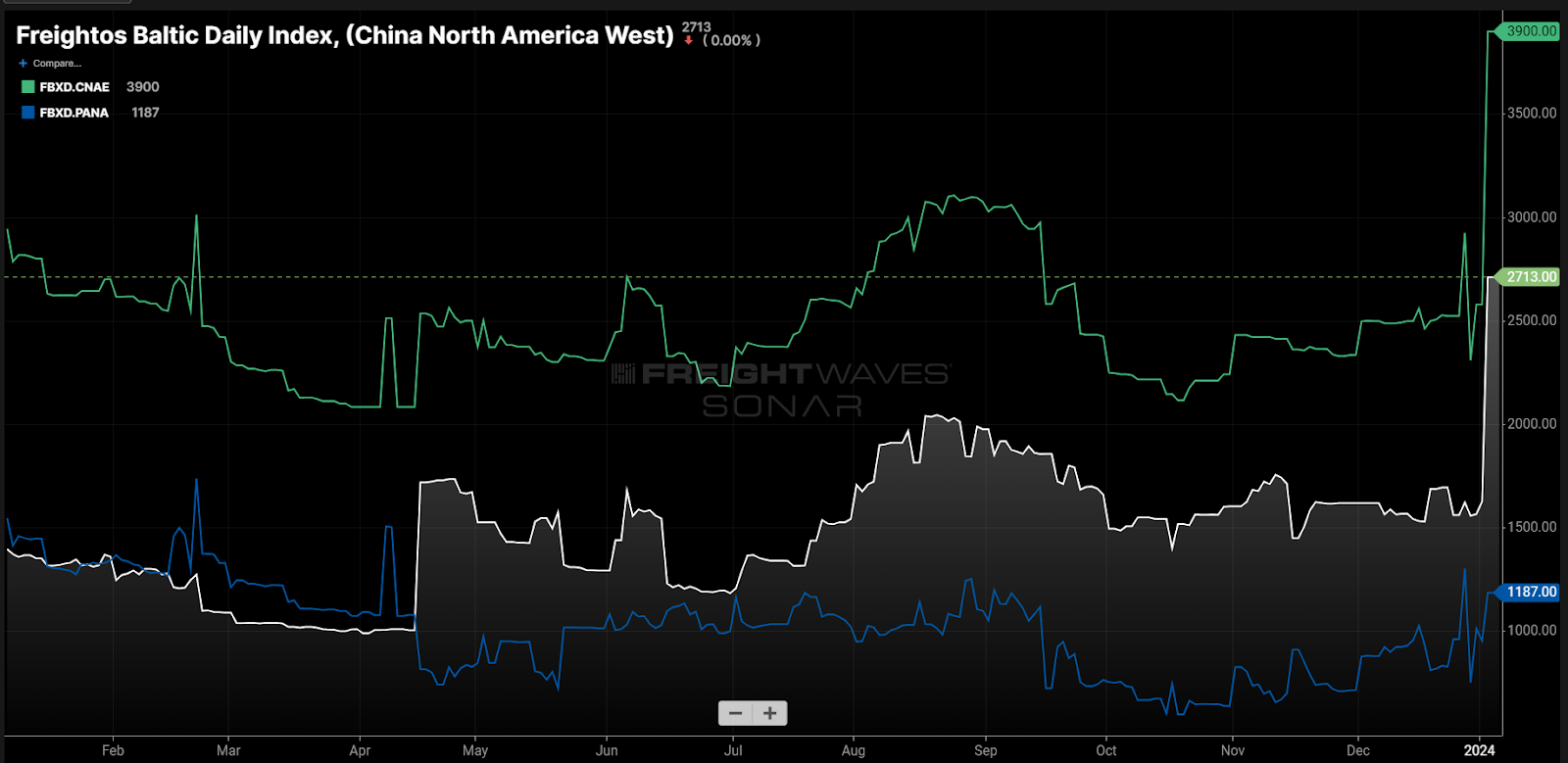

Chart of the Week: Freightos Baltic Each day Index – China to North American west and east coasts, Panama Spread SONAR: FBXD.CNAW, FBXD.CNAE, FBXD.PANA

Disproportionate shipping rate increases resulting from the Red Sea attacks further incentivize shippers to bring freight into the U.S. West Coast from Asia, as a pandemic-era pattern of shipping to Eastern ports continues to unwind.

Spot rates for 40-foot equivalent containers moving on the ocean from China to North America’s east and west coasts spiked, based on the Freightos Baltic Exchange indices, to start out the 12 months. The conflict within the Middle East is now impacting nearly all global shipping lanes. Inbound east coast rates increased greater than those to the west, increasing the “Panama Spread” back over $1,100.

The Panama Spread measures the difference between maritime container shipping rates from China to the North American east and west coasts. More positive figures indicate a stronger monetary incentive to ship to the west coast.

The continuing drought in Central America has restricted the flow of freight moving through the Panama Canal and has increased transit times.

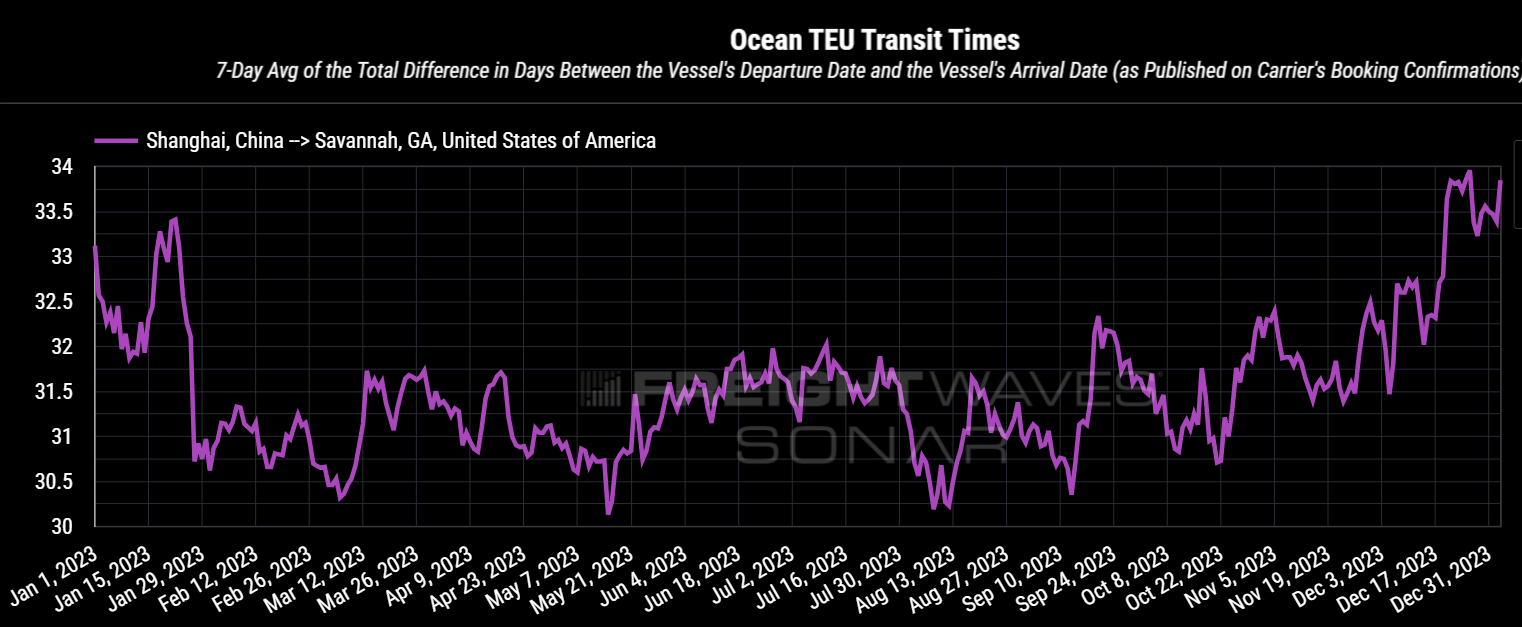

Transit times from Shanghai to the Savannah, Georgia, port have increased nearly 2.5 days since October, based on SONAR’s Container Atlas, as canal capability was limited on account of a scarcity of water.

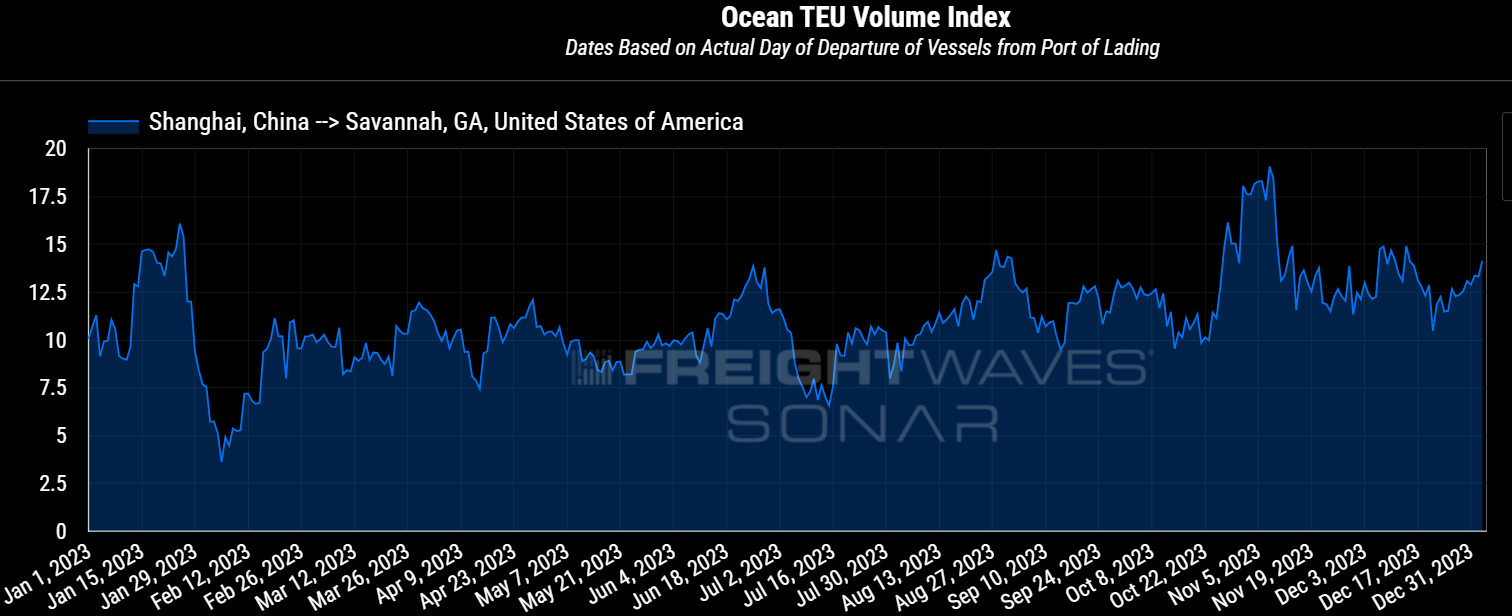

Thus far demand doesn’t seem like impacted by the increasing service. Booking volumes within the Shanghai-to-Savannah lane are up for the reason that restrictions were placed on the canal. Time will tell if the speed increases will persist and erode demand.

U.S. import demand has increased at a sustainable rate over the past 12 months as inventories appear to have right-sized, increasing the necessity for more consistent replenishment.

A surprisingly robust consumer has also contributed to stronger-than-expected import demand.

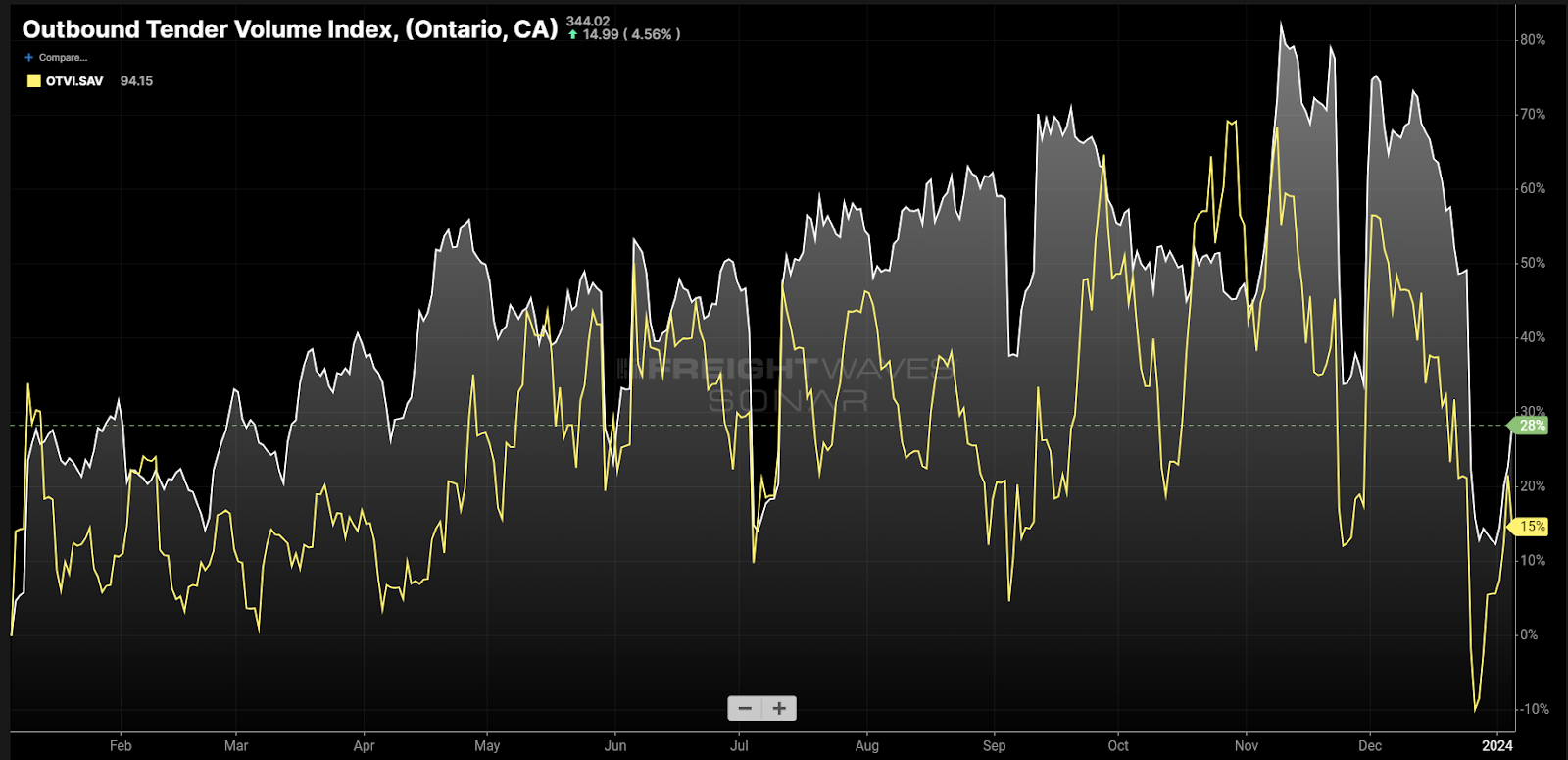

It’s difficult to inform with any precision how much influence the increased transit times and value differentials have had on domestic freight. Tender volumes out of two of the country’s most import-dependent markets — Ontario, California, out West and Savannah within the East—have increased over the past 12 months, with the Western market growing greater than the Eastern one.

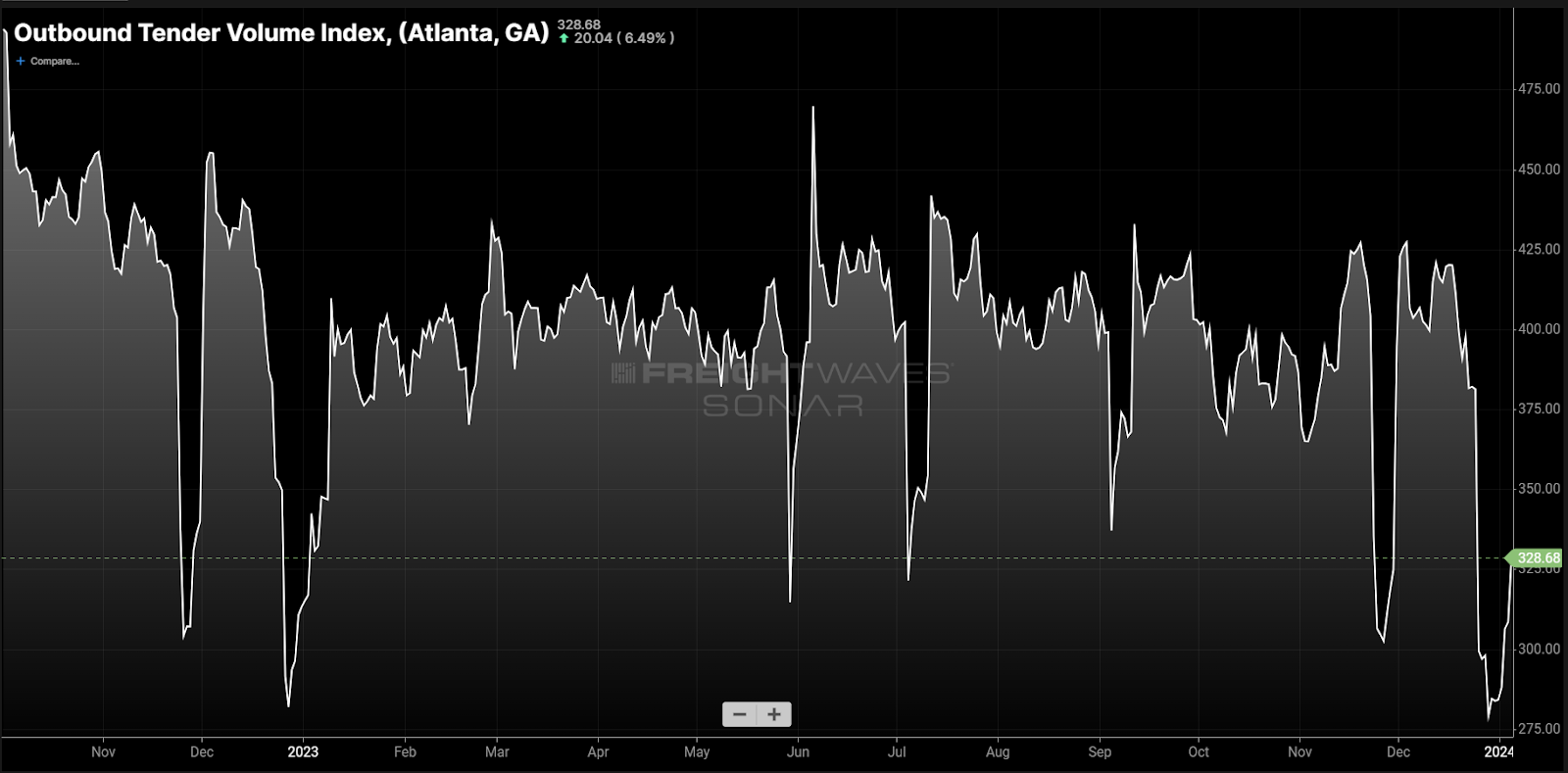

The Atlanta market — the second-largest outbound freight market within the country, with strong ties to Savannah — has not grown, with tender volumes contracting from an annual perspective.

The Southern California freight markets are likely to slow in January and February before ramping within the spring and peaking around September.

Freight attrition can be difficult to acknowledge at this point because the domestic truckload market stays heavily oversupplied with capability, but many predict that to alter later within the 12 months.

The Los Angeles-area markets were the bottleneck for a lot of supply chains throughout the pandemic. On the bare minimum, recent events are pushing more volume to the West, which could manifest more significantly later this 12 months.

Concerning the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from hundreds of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, survive the front page. After that, the Chart of the Week can be archived on FreightWaves.com for future reference.

SONAR aggregates data from a whole lot of sources, presenting the info in charts and maps and providing commentary on what freight market experts need to know in regards to the industry in real time.

The FreightWaves data science and product teams are releasing latest datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post What the Red Sea conflict means for domestic transportation appeared first on FreightWaves.