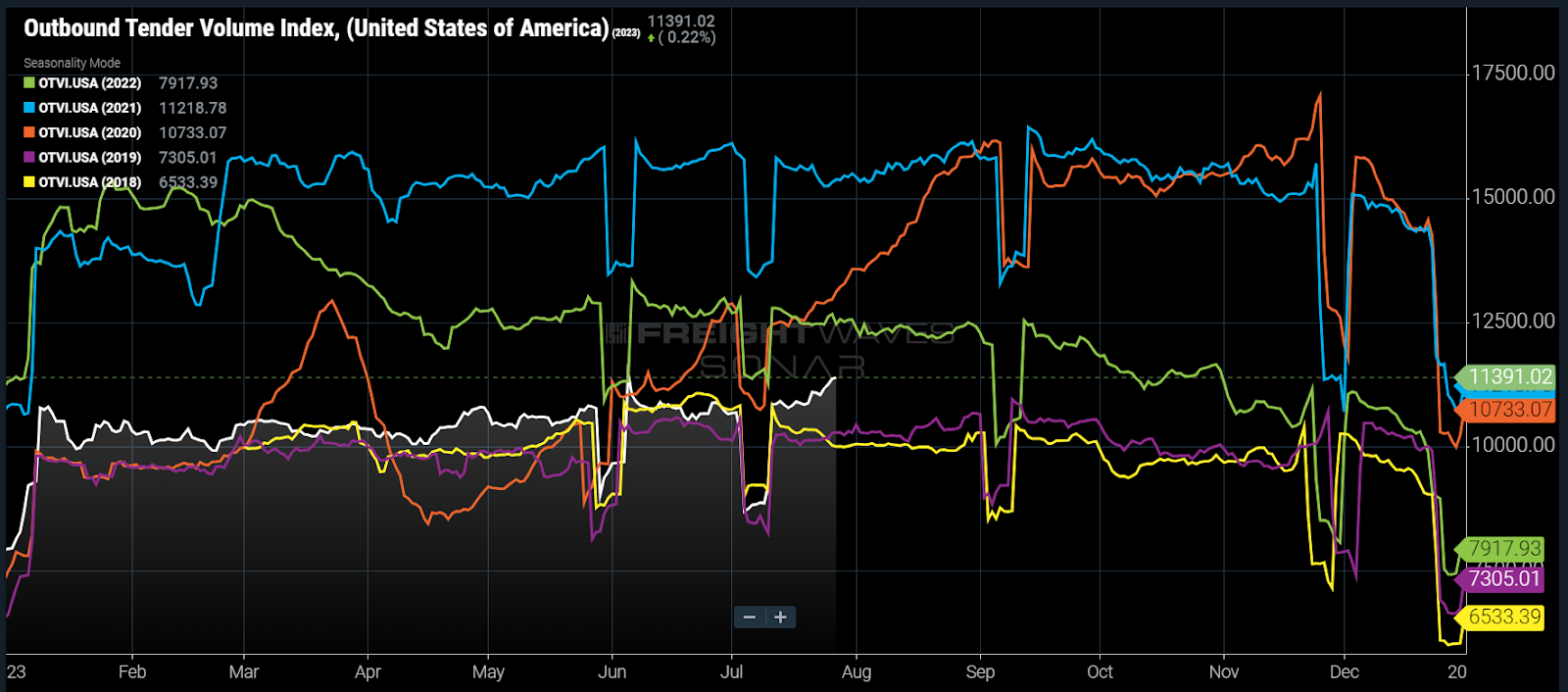

Chart of the Week: Outbound Tender Volume Index – USA SONAR: OTVI.USA

After what has felt like a relentless barrage of bad news, an unseasonable upward trend in truckload tender volumes is giving domestic transportation providers the potential inflection point they’ve desperately been waiting for.

The national Outbound Tender Volume Index (OTVI) — a measure of the electronic requests for truckload capability from shipper to carrier — is up nearly 7% versus month-ago levels. It is a complete break from tradition — excluding the pandemic-fueled rise in 2020.

A typical summer pattern has tender volumes rise slowly from mid-May to the top of June after which fall back in July. In 2018, tender volumes fell 7% through the month of July; 2019 had a way more moderate 2-3% drop.

The fundamental story of the trucking market has been one among abundant capability after demand collapsed last yr. Tender volumes fell roughly 17% from early March to late April of 2022. Demand leveled off throughout the summer before resuming a slower-paced decline within the second half of the yr, falling roughly one other 16%.

Through the primary half of 2023 there have been few surprises from the OTVI because it has followed a more traditional path after appearing to bottom at a worth of 9,940 in February after which climbing 8% higher by the top of June. The pre-pandemic years of 2018 and 2019 had similar increases.

Rates still falling

The jump in July demand has had no impact on either tender rejection rates or the spot market. Capability stays abundant and able to handling the unseasonable surge for essentially the most part. The national Outbound Tender Reject Index (OTRI) fell from a July 1 peak value of three.89% to 2.9% on July 18. It rose to three.23% by Thursday, which is marginal at best.

The National Truckload Index (NTI), which measures spot rate trends, has dropped 4.3% since July 6 with no signs of fixing course.

Anticipated disruptions

While nearly unattainable to inform the precise reason for the bizarre strengthening in demand, there’s credence to the speculation that the recent labor disputes around LTL provider Yellow and UPS can have spurred some activity from the shipping community to attempt to get in front of or take care of any potential service disruptions which will result from either provider ceasing service.

The past few years are still relatively fresh on the minds of transportation and provide chain managers who directly felt the repercussions of a market through which capability tightened quickly. An oz of precaution is value a pound of cure.

Early replenishment

While the expansion has been relatively dispersed across the country, the West Coast is liable for the majority of the rise and subsequently long-haul dry van demand has also had the strongest jumps.

This might simply be an early “peak season” for freight replenishment that normally occurs in September and October. With rates on the ground, some shippers could also be making the most of a stable environment with the long run still uncertain. This might require a return to confidence of their demand planning, something that has been largely absent since 2020, however it does line up with the present maritime narrative.

Each of the aforementioned theories can be a short-lived event for the freight market. A more sustainable cause requires economic support, which is difficult to seek out amid a weakening consumer environment.

Government spending to the rescue

There’s little reason to expect growth from the retail or housing markets. The automotive sector is starting to point out signs of slowing as well. Government spending from the infrastructure bill could finally be having an impact as bridge and tunnel investment is trending significantly higher, however it is difficult to make that reference to long-haul dry van freight.

In fact, there doesn’t must be one easy reason because it might be a mixture of multiple things. Transportation providers should take the present situation as a near-term win but remain cautious. If anything, this break in seasonal trend shows that we’re still in a comparatively unpredictable environment.

Concerning the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from 1000’s of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, continue to exist the front page. After that, the Chart of the Week will probably be archived on FreightWaves.com for future reference.

SONAR aggregates data from a whole lot of sources, presenting the information in charts and maps and providing commentary on what freight market experts need to know in regards to the industry in real time.

The FreightWaves data science and product teams are releasing recent datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post Unseasonable rise in demand provides much-needed optimism for transportation providers appeared first on FreightWaves.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/F5ERKB2GSZC7DOSER4SCJDZVSQ.jpg)