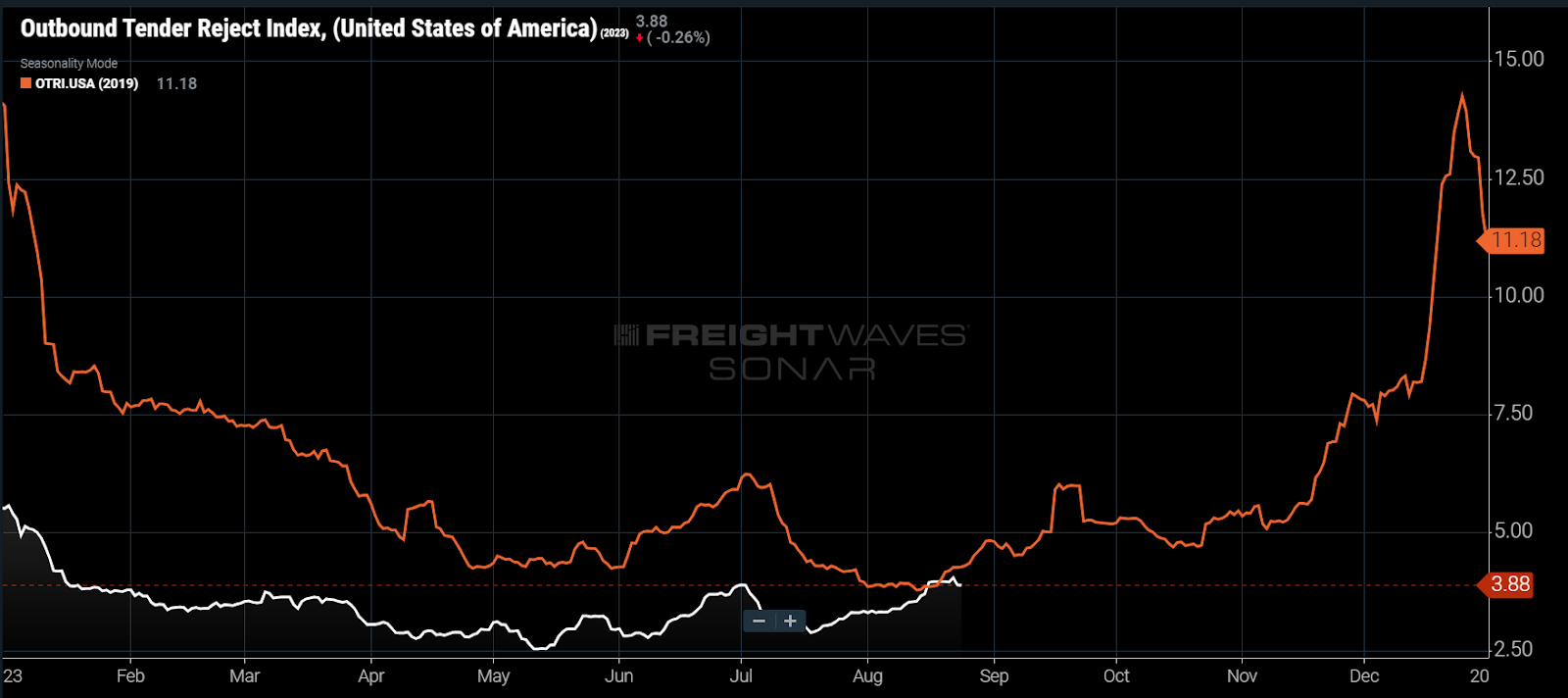

Chart of the Week: Outbound Tender Reject Index – USA SONAR: OTRI.USA 2023 v 2019

The national Outbound Tender Reject Index (OTRI) topped 4% this month for the primary time since early January, when it was recovering from the vacation period. While 4% continues to be indicative of a really loose market, the timing and direction of the OTRI are signaling that the softest conditions could also be within the rearview mirror.

The recent bump can be the primary time the OTRI has moved above the worth of 2019, when there was a historically loose market with significant carrier exits. The 2019 values do offer some historical support for increasing rejection rates, but this rise is about two to a few weeks sooner than expected.

The national OTRI measures the speed at which carriers reject loads from shippers under a previously agreed upon or contracted rate. Typically, values below 4.5% are connected to truckload markets with abundant capability and are deflationary for contract rates.

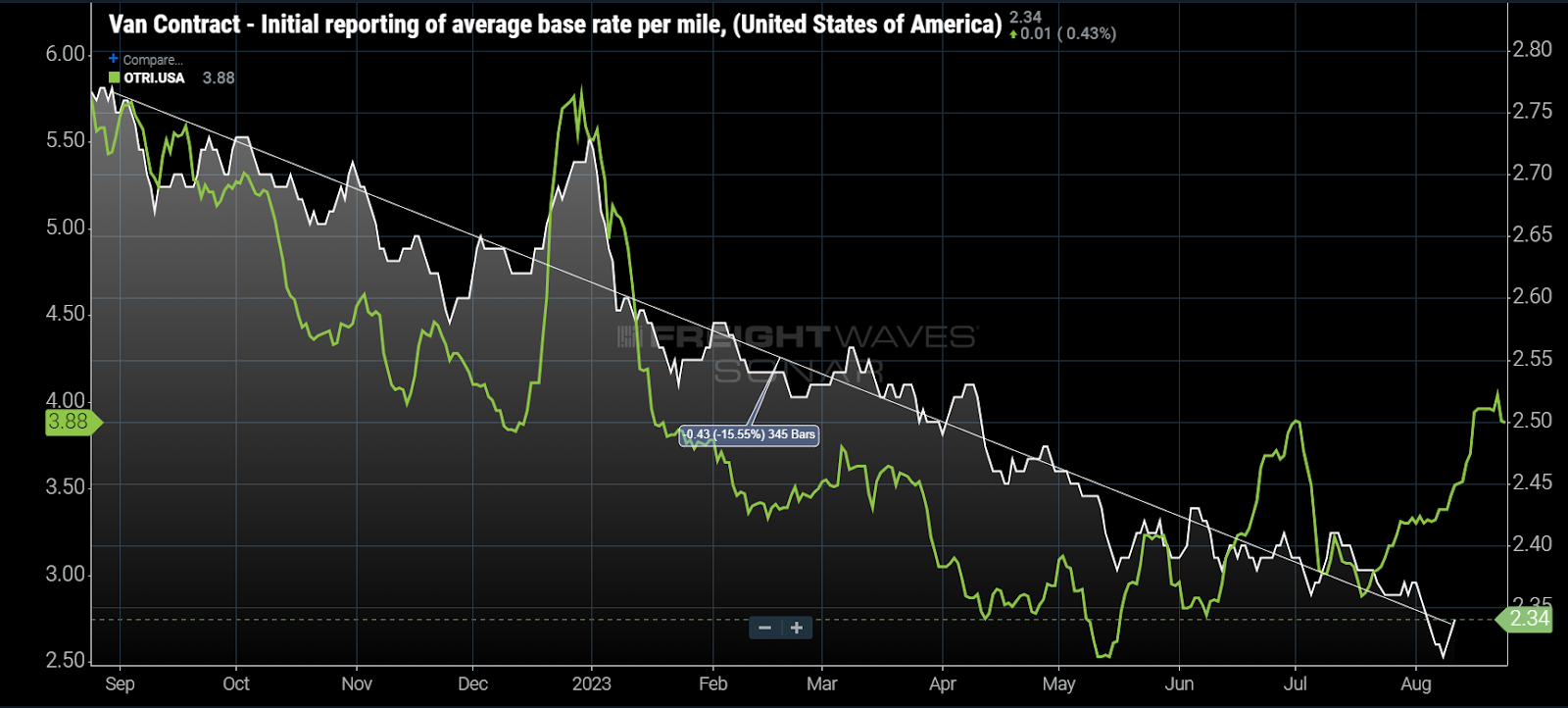

Contract rate competition

The race to the underside can have finally caught as much as shippers as carrier margin erosion has now made prioritizing load decisions a little bit tougher. In a high-margin contract rate environment, like in 2022, all loads earn a living and the one concern is coverage. With ORs shrinking and margins falling, carriers now need to also consider which loads are more financially lucrative.

The OTRI has been below 4% nearly all yr, averaging 3.2% from February through July. Subsequently, dry van contract rates have fallen roughly 15% over the past yr. The recent rise in OTRI — jumping from 3.3% to 4% — seems to align perfectly with a robust dip in average contract rates in early August. This means that carriers are seeing a slight increase in optionality when selecting loads.

This connection could also be somewhat spurious, as there are other aspects at play available in the market, like an unusually strong increase in long-haul demand this July, nevertheless it is definitely a contributing factor as rates fall closer to breakeven levels.

The domestic freight market experienced nearly a yr and a half period of overheating in 2020-2021, creating an economic bubble for the sector. It has taken nearly a yr to tug contract rates right down to a level that carriers are a minimum of not only auto accepting the whole lot that comes their way.

While an increase in rejections from 3% to 4% will not be that significant, the longer trend line, the recent jump is a component of an prolonged period of accelerating rejections starting in May, when one other strong dip in contract rates occurred.

Early replenishment

Most of the nation’s largest retailers import their goods into the port complexes of Los Angeles and Long Beach and stage them there before shipping them across the country. The height of this activity typically occurs in September through November. It appears to have began early this yr.

Increasing load volumes out of the West could also be disrupting carrier networks as they struggle to reposition equipment across long distances. Southern California is home to considered one of the most important warehousing districts within the U.S., colloquially known as the Inland Empire.

Rejection rates have risen above the national average out of the Los Angeles market this summer after spending the previous yr and a half well below the national OTRI.

Whatever the reasons, the freight market is showing an elevated level of responsiveness that has been absent for over a yr. While that is under no circumstances the tip to what looks like a freight drought for transportation providers, it is an indication that the market is popping more of their direction as the standard peak season approaches.

Concerning the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from hundreds of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, live to tell the tale the front page. After that, the Chart of the Week can be archived on FreightWaves.com for future reference.

SONAR aggregates data from tons of of sources, presenting the info in charts and maps and providing commentary on what freight market experts need to know concerning the industry in real time.

The FreightWaves data science and product teams are releasing latest datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post Truckload capability tightens in August appeared first on FreightWaves.