Truckload carriers and 3PLs have seen little change in demand halfway through the fourth quarter, and a few are pointing deeper into 2024 before the market corrects.

The comments got here from heads of a number of the largest publicly traded TL providers at Stephens twenty fifth Annual Investment Conference in Nashville, Tennessee, on Tuesday. The sentiment aligns with a Tuesday report from freight payments platform Cass Information Systems (NASDAQ: CASS), which said October produced a cycle low for shipments.

Freight broker Landstar System (NASDAQ: LSTR) said the market is a little bit softer than it was at the tip of October when it reported third-quarter earnings and provided fourth-quarter guidance. The corporate said it doesn’t expect a peak season this 12 months.

“There’s no excitement on the market — whether it’s the parcel carriers, the shippers — or anybody who thinks this thing goes turn anytime soon,” said Jim Gattoni, Landstar president and CEO.

He said sequential seasonal patterns have been lower than normal in every month of 2023. He reiterated the corporate’s fourth-quarter outlook but now expects results to shake out closer to the center or the lower end of the range.

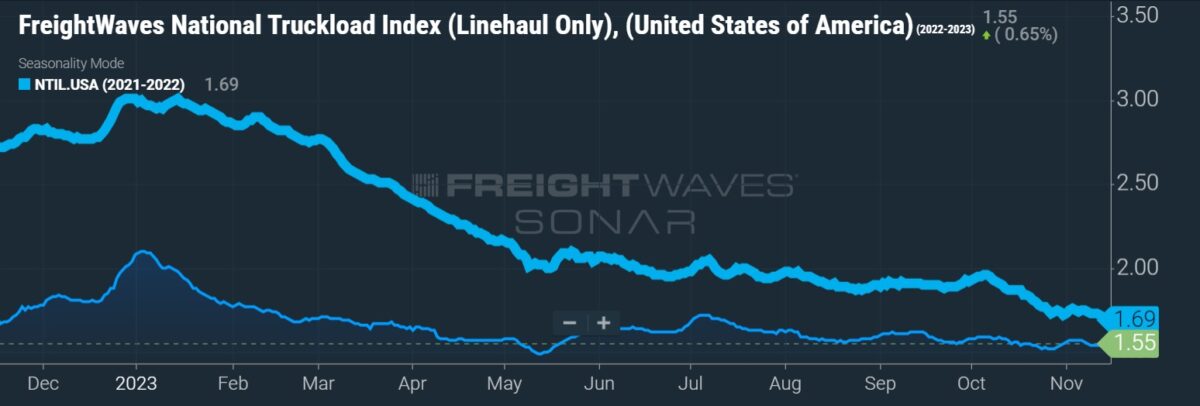

He doesn’t see spot rates stepping materially higher until next 12 months and said that it often takes higher demand versus capability attrition to maneuver the market. Turnover amongst Landstar’s business capability owners, a proxy for truck capability, is 39% this 12 months, which is consistent with the 36% rate recorded throughout the 2019 downturn.

“We’re continuing to tug down,” Gattoni said about spot rates. “But I feel by the point we get into 2024, possibly midsummer, we’ll start seeing regular seasonal patterns again.”

Management from TL carrier Werner Enterprises (NASDAQ: WERN) noted a “fairly muted” peak season. It said volumes have been regular to barely higher than last 12 months’s peak but pricing has been weaker, leading to lower revenue 12 months over 12 months (y/y).

The corporate has seen “no surprises to the negative” since its Nov. 1 earnings report. Nevertheless, it noted the subsequent 4 weeks are very necessary to the fourth-quarter result. Werner didn’t provide a pricing outlook for next 12 months but said that its contract rates have already fully reset lower and an elevated cost structure means “there isn’t much to present” at the same time as inflation moderates.

Werner’s fourth-quarter outlook calls for revenue per total mile in its one-way segment to be flat to barely down from the third quarter but off 7% to 9% y/y. Revenue per truck per week in its dedicated unit is anticipated to complete 2023 flat to up 3% y/y. Werner said it should proceed to give attention to cost control but didn’t provide a timeframe for an eventual turnaround.

“History has indicated that it won’t take much of a blip in demand together with the continued decrease in supply … . The ‘when’ is difficult to say,” said Craig Callahan, Werner’s chief business officer.

Multimodal provider J.B. Hunt Transport Services (NASDAQ: JBHT) provided a more upbeat tone, at the least for its intermodal segment.

The corporate has been seeing record intermodal volumes in its network in recent weeks, noting the unit is often the one which first sees a turn when exiting a recession.

“We knew we were taking share,” said Shelley Simpson, J.B. Hunt president, when discussing the positive inflection that had just began to occur when it reported third-quarter results a month ago. “I don’t think we understood the magnitude of the share that we were taking.”

She said she was pleased with intermodal peak season but didn’t provide any direction on intermodal pricing. J.B. Hunt’s recent intermodal bid season concluded within the third quarter, and Simpson said “we’ll live with that pricing” throughout the fourth and first quarters. She believes it should take a while for the recent volume surge to push rates higher.

“We all know what the inflation is and we’re not satisfied with our margins,” Simpson said. “Now we’re all the way down to the timing of when can we get appropriate returns and appropriate price from our customers.”

Demand in the corporate’s truckload segments has been more reflective of a freight recession. Nevertheless, its dedicated unit is seeing a slowdown within the variety of accounts saying they need fewer trucks.

Most of its customers have worked through excess inventories, but they continue to be uncertain about future demand.

“Our customers don’t see a big downturn,” Simpson said. “I feel they feel OK about 2024. I feel our customers are in a more neutral to barely positive position.”

Schneider National (NYSE: SNDR) has also seen positive intermodal trends recently but categorized the broader freight market as “unseasonably tepid.”

“We did see a little bit little bit of bounce because it pertains to intermodal volumes, particularly within the month of October,” said Mark Rourke, president and CEO. “We want to see some endurance there before we claim any real victories.”

- October shipments hit cycle low, Cass says

- Forward’s recent long-term targets don’t include Omni

- Annual LTL GRIs barely ahead of schedule

The post Trucking heads kick can further into 2024 appeared first on FreightWaves.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/TCIQQJM5RRHSJMHIWL7VR2L3BI.jpg)

{kind=link}