Chart of the Week: National Truckload Index Linehaul Only, Outbound Tender Rejection Index – USA SONAR: NTIL.USA, OTRI.USA

The typical dry van truckload spot rate excluding the estimated cost of fuel (NTIL) has increased 4.2% for the reason that end of April, while carrier contracted load rejection rates are still near all-time lows. While overall capability continues to be extremely loose, some areas of the country have seen increasing spot rates and underlying freight flows proceed to shift.

The NTIL bounced off a worth of $1.50 in early May, rising to a current value of $1.64, with FreightWaves’ forecast value showing upward pressure heading toward the Fourth of July. The national Outbound Tender Rejection Index (OTRI) has bounced between 2.5% and three.2% during that very same time, which doesn’t appear to support the spot rate movement.

It just isn’t the primary time that the spot market has seemingly grow to be disconnected from the contract market, but has it really?

Rates are noisy

The primary component as to why rejection and spot rates moved in a unique direction is the straightforward fact rates are measuring greater than capability availability. Carrier costs are the biggest component of rates more often than not, but these are relatively static and don’t contribute much to rate volatility.

Market sentiment is probably the most volatile and in addition probably the most difficult component of spot rates to quantify. This is predicated on how strongly a shipper needs to maneuver a load and perceived carrier availability. Neither of this stuff are objective, which is why the market might be irrational in times of transition. That is an oversimplification for certain, but one could write a whole dissertation on market pricing dynamics.

Freight flow is unbalanced

The fee of positioning a truck can also be included in lots of rates, especially in lanes where the destination is oversupplied with capability. Some amount of this is comparatively static based on the natural flow of freight within the U.S. being relatively consistent over time, but that appears to have modified. An aggregate shift on this component can trigger a change in market sentiment.

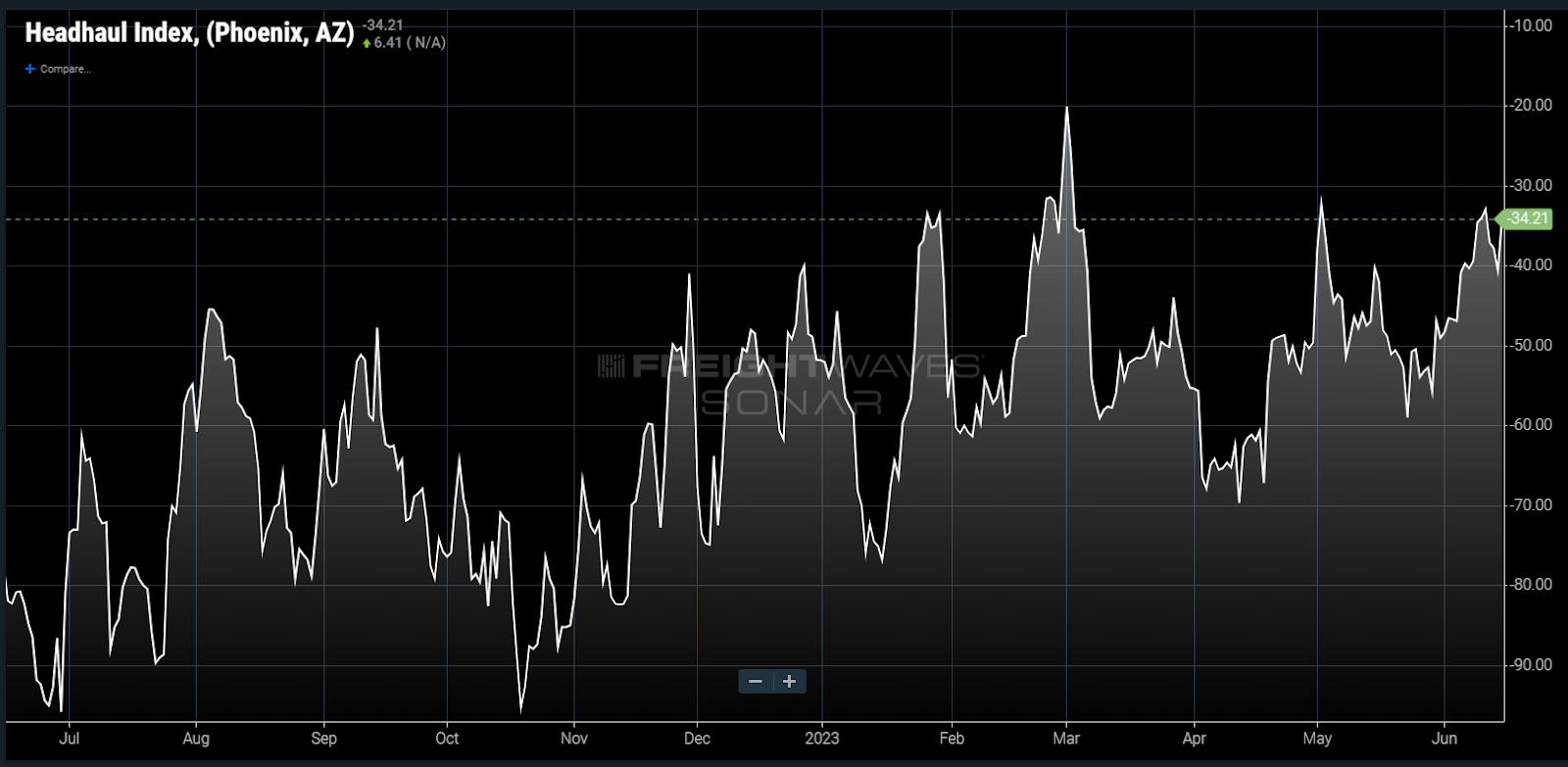

The Phoenix market is a very good example of where there was significant outbound demand growth relative to inbound. Outbound tender volumes (shipper requests for capability) are averaging 4% higher yr over yr over the past month, while inbound tender volumes are down 14%.

The FreightWaves Headhaul Index (HAUL) measures outbound less inbound tender volumes at a market level and shows Phoenix moving from an especially inbound-heavy market to much less of 1 over the past yr. Negative values indicate more inbound than outbound.

The incontrovertible fact that this trend didn’t occur overnight makes it relatively difficult to see. Smaller operators have less visibility of general market trends and so that they typically are later to make adjustments. This may very well be a reason spot rates have been on the rise out of Phoenix, while tender rejections have only increased marginally.

Contract continues to be king

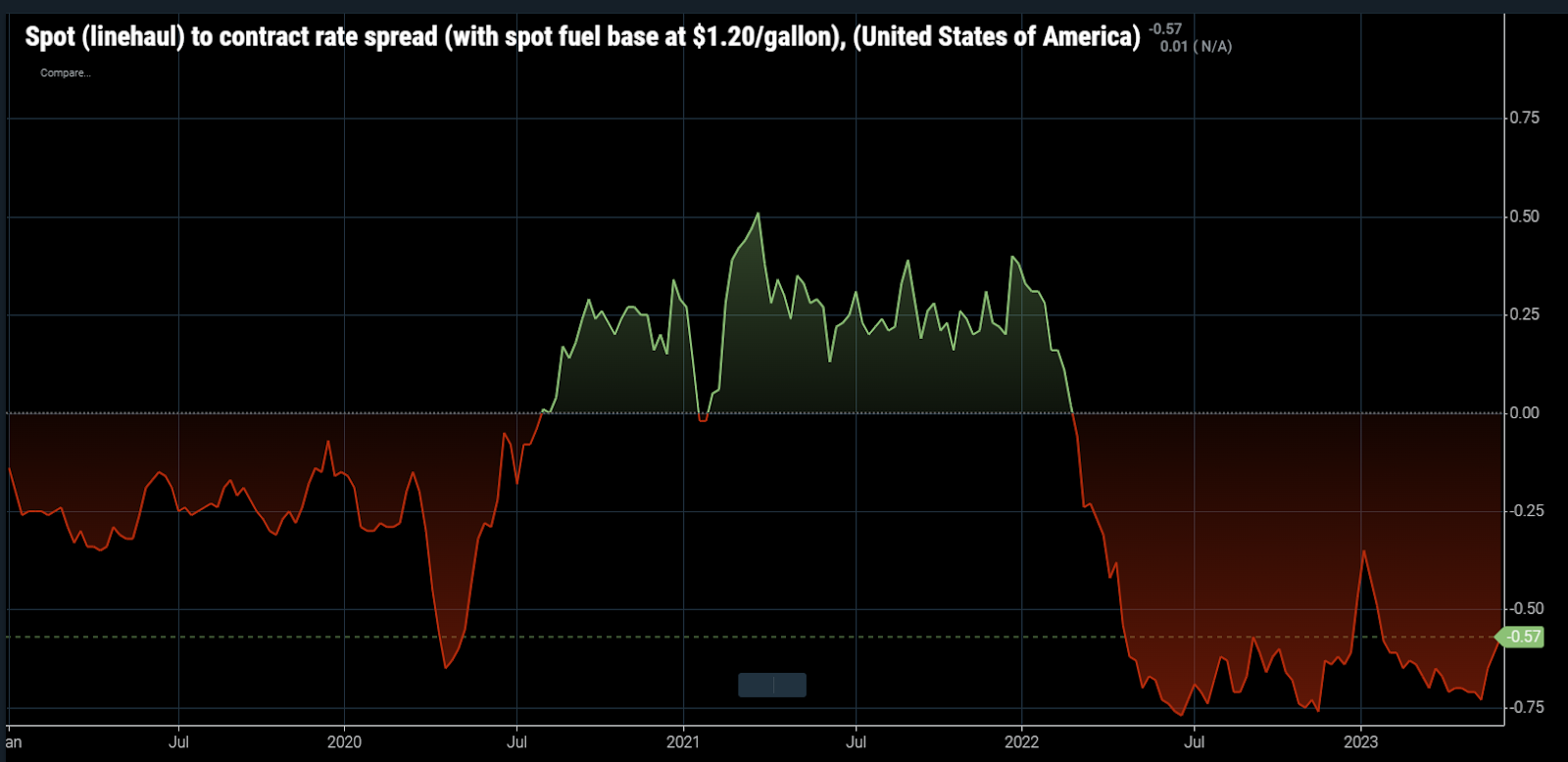

Perhaps the strongest reasoning behind the apparent discrepancy between tender rejections and spot rate is the incontrovertible fact that contract rates are still averaging well above spot.

Spot rates excluding an estimated cost of fuel above $1.20 per gallon (with a view to make them comparable to contract rates less an ordinary fuel surcharge) are still showing a deep discount in comparison with contract rates. The red lines on the chart show periods where the national average spot rate is below contract.

Contract rates move much slower than spot rates attributable to the character of their long-term agreements. Their continued elevation relative to identify signifies that rising spot rates will not be going to tempt carriers to divert capability to the spot market with a view to chase higher margins.

While this may increasingly not be the inflection point many transportation providers are hoping for by way of a market shifting to a more balanced state between demand and provide of capability, it is a sign that the spot market may grow to be more reactive as capability corrects throughout the remaining of the yr.

The dearth of rise in rejection can also be an indication that the perceived market instability might be short lived as carriers recognize and shift capability where it is required.

In regards to the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from hundreds of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, live to tell the tale the front page. After that, the Chart of the Week might be archived on FreightWaves.com for future reference.

SONAR aggregates data from lots of of sources, presenting the information in charts and maps and providing commentary on what freight market experts need to know concerning the industry in real time.

The FreightWaves data science and product teams are releasing recent datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Way forward for Supply Chain

JUNE 21-22, 2023 • CLEVELAND, OH • IN-PERSON EVENT

The best minds within the transportation, logistics and provide chain industries will share insights, predict future trends and showcase emerging technology the FreightWaves way–with engaging discussions, rapid-fire demos, interactive sponsor kiosks and more.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/F5ERKB2GSZC7DOSER4SCJDZVSQ.jpg)

{kind=link}