Enterprise version of Skydio X10

Drone Industry Insights has published their latest report detailing the state of Drone Industry Investments. The research is an in-depth evaluation: but one stark fact stands out within the summary. Within the realm of drone industry funding, the 12 months 2023 witnessed a notable downturn, marking a departure from the meteoric rise seen in previous years.

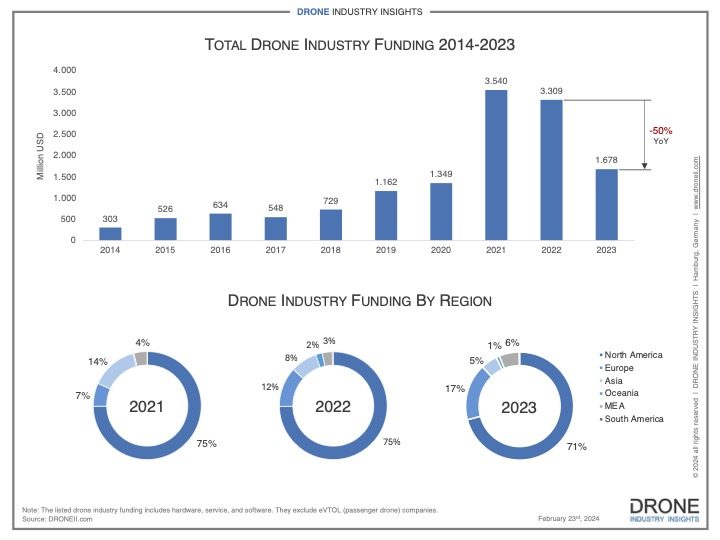

Data gleaned from investment infographics and the blog post by Zahra Lotfi reveals that the cumulative total of funding for drone corporations worldwide in 2023 stood at US$1.7 billion. While this figure may appear substantial at first glance, it pales compared to the previous 12 months’s total of US$3.3 billion, signifying a stark decline.

An evaluation of funding patterns sheds light on several key aspects contributing to this downturn. One significant aspect is the shifting landscape of enterprise capital investments, particularly in later-stage funding rounds. Across various industries, including drones, there was a noticeable decrease in the worth of such investments. This trend suggests that corporations transitioning past the startup phase may encounter greater challenges in securing substantial financial backing.

Furthermore, the landscape of initial public offerings (IPOs) and post-IPO deals presents a mixed picture. While the worth of those transactions has greater than doubled, indicating a positive trajectory for corporations entering financial markets, there was a discount within the variety of such deals in comparison with the previous 12 months. This dichotomy underscores the nuanced nature of the funding landscape, defying easy categorization as wholly positive or negative.

Regionally, North America emerged as the first beneficiary of drone company funding, capturing 71% of the worldwide total. Major investments in corporations like Zipline and Skydio bolstered the region’s position as a key player within the industry. Nonetheless, the share of funding allocated to North America has declined since 2021, while Europe has seen a gradual increase, accounting for 17% of worldwide funding in 2023.

The distribution of funding across industry segments also offers insights into prevailing trends. Hardware corporations proceed to receive a better percentage of investments, reflecting the numerous costs related to manufacturing drone platforms. Nevertheless, there was a notable shift in funding towards drone service corporations, surpassing investments in drone software corporations—a reversal from the previous 12 months.

As stakeholders ponder the implications of those funding dynamics, questions arise regarding the trajectory of the drone industry. Is the decline in funding indicative of a broader shift towards emerging technologies equivalent to Advanced Air Mobility (AAM)? Or does it signify a natural progression because the industry matures? With these considerations in mind, stakeholders are poised to navigate the evolving landscape of drone industry funding, adapting strategies to capitalize on emerging opportunities and address underlying challenges.

Despite the stark difference in investment between 2022 and 2023, Lotfi sees room for optimism within the numbers:

“The economic shocks and major financial impact of the COVID-19 pandemic in 2020-2021 led to astoundingly high investments in drone technology (where investment values greater than doubled). But when these outlier years are factored out, drone company funding would still show a continuous upward trend since 2017,” she writes. “Furthermore, deep technologies equivalent to artificial intelligence and machine learning are trending upward at an incredible rate, and these have a direct impact on drone technology. Perhaps these will even create a singular opportunity to take a position in drone corporations very similar to the pandemic did, except this time the regulatory progress will even be more palpable.”

{kind=link}