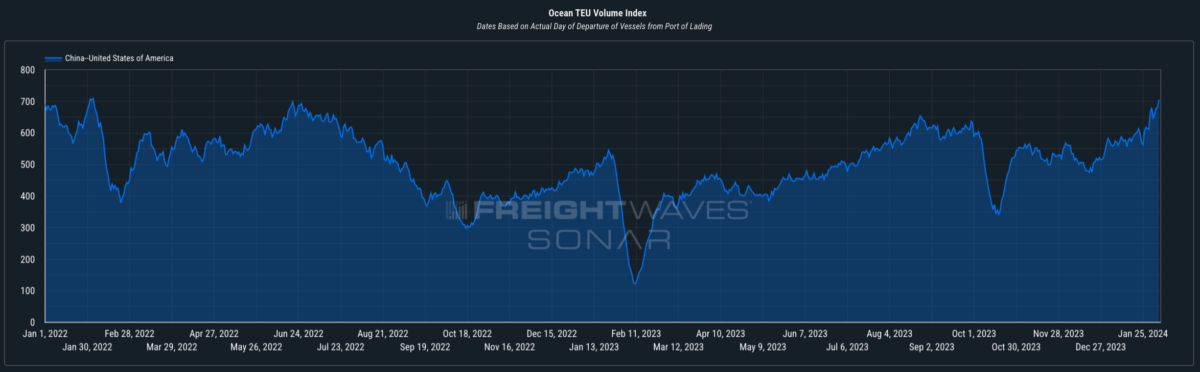

There’s a seeming contradiction within the macroeconomic and trade data coming out of China nowadays: Despite contracting industrial activity, low consumer confidence and a worsening stock market rout, China is currently sending the very best volume of ocean container freight to the USA since May 2022.

A part of the surge in shipments is attributable to the normal pre-Chinese Recent Yr surge, when factories on China’s coast move a flurry of products to the port before their staff depart for an extended holiday of their hometowns. But this 12 months’s peak is well above 2023’s anemic Chinese Recent Yr season, and volumes have been mounting all 12 months.

Container volumes from China to the USA are steadily growing at a time when the macroeconomic picture in China couldn’t be more uncertain. China’s manufacturing Purchasing Managers’ Index contracted in January for the fourth consecutive month. China’s second-largest property developer, Evergrande, is being liquidated, with roughly $300 billion in debts against $245 billion in assets. Chinese stocks have been in a deepening rout: The CSI 300, an index of the 300 largest stocks on the Shanghai stock exchange, is down greater than 19% over the past 12 months. The Chinese government has taken steps to limit short selling by domestic institutional investors and is considering asset purchases exceeding $1 trillion with a purpose to put a floor under the market.

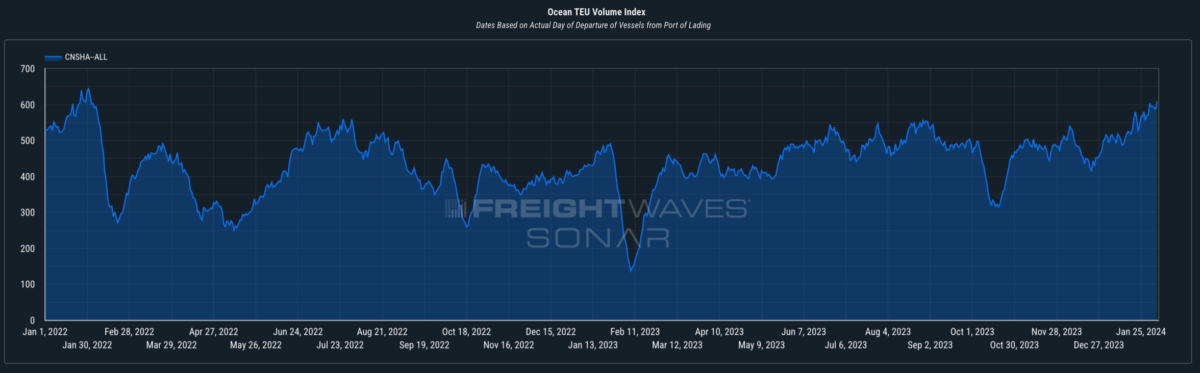

Why, if China’s GDP growth fell to five.3% in 2023, its slowest growth of the twenty first century, is the port of Shanghai (for instance) shipping more volume than at any time previously two years?

It seems that volume isn’t a lot being out of China by a burgeoning manufacturing sector a lot because it’s being out of China by U.S. importers who’ve burned off inventory and are preparing to face higher-than-expected retail sales. In November 2023, essentially the most recent date for which data is on the market, U.S. inventory-to-sales ratios fell to 1.37 months, well below pre-pandemic baselines. Meanwhile, in December 2023, U.S. retail sales grew 4.8% 12 months over 12 months to $709 billion, outpacing overall y/y GDP growth of three.3% within the fourth quarter of 2023.

February and March must be relatively strong months for U.S. ports, particularly on the West Coast. Basically, when inventories are low yet economic growth is robust, transportation providers find themselves in a more favorable business environment. Retailers and manufacturers must move higher volumes of products and speed up the rate of freight through their networks, which tightens transportation capability and raises rates.

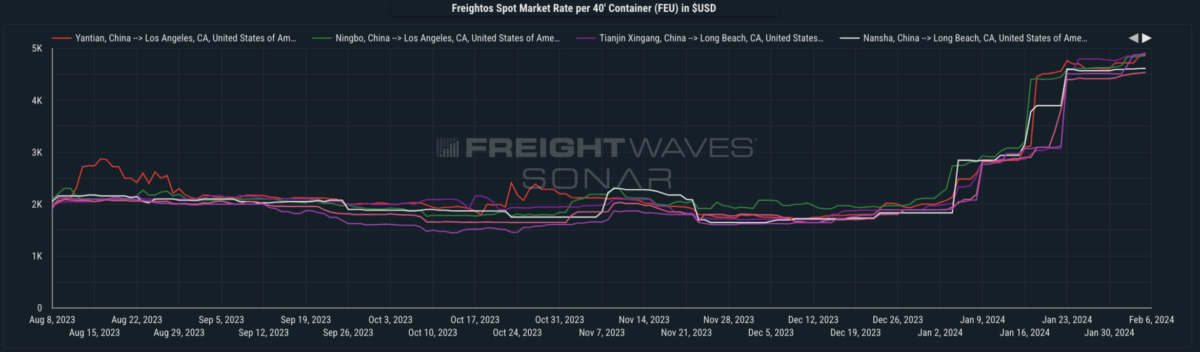

On the opposite side of the planet, Houthi terrorist attacks against international shipping within the Red Sea have necessitated diverting shipping from the Suez Canal across the Cape of Good Hope, extending transit times and effectively removing containership capability from the market. Because those strains on steamship line networks are coinciding with higher volumes out of China, eastbound spot rates on the trans-Pacific have ripped upward to greater than $4,500 per forty-foot equivalent unit on most lanes out of China to the West Coast.

In C.H. Robinson’s fourth-quarter earnings call on Jan. 31, CEO Dave Bozeman commented on the crisis’ impact on global supply chains and container rates.

“Within the wake of the continued conflict within the Red Sea and low water levels within the Panama Canal, global supply chains are facing transit interruptions and vessel rerouting, which is causing prolonged transit times and putting a strain on global ocean capability,” Bozeman said. “While the Asia-to-Europe trade lane has been most affected, the impact is extending to other lanes as carriers adjust routes based on shipping demand. Consequently, ocean rates have increased sharply in Q1 on several trade lanes, including Asia to Europe and Asia to North America. While the Red Sea disruption continues with none clear timeline of when it would be resolved, the strain on capability and the elevated spot rates are expected to proceed through a minimum of the Chinese Recent Yr.”

In response to the Port of Los Angeles’ PortOptimizer, Week 6 TEU volumes were up 38.6% in comparison with the identical week in 2023 (105,076 TEUs vs. 75,801 TEUs). In other words, volumes are already elevated in comparison with last 12 months, and there’s reason to consider that much more is on the best way.

The post Despite economic worries, more containers flow from China to US appeared first on FreightWaves.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/F5ERKB2GSZC7DOSER4SCJDZVSQ.jpg)

{kind=link}