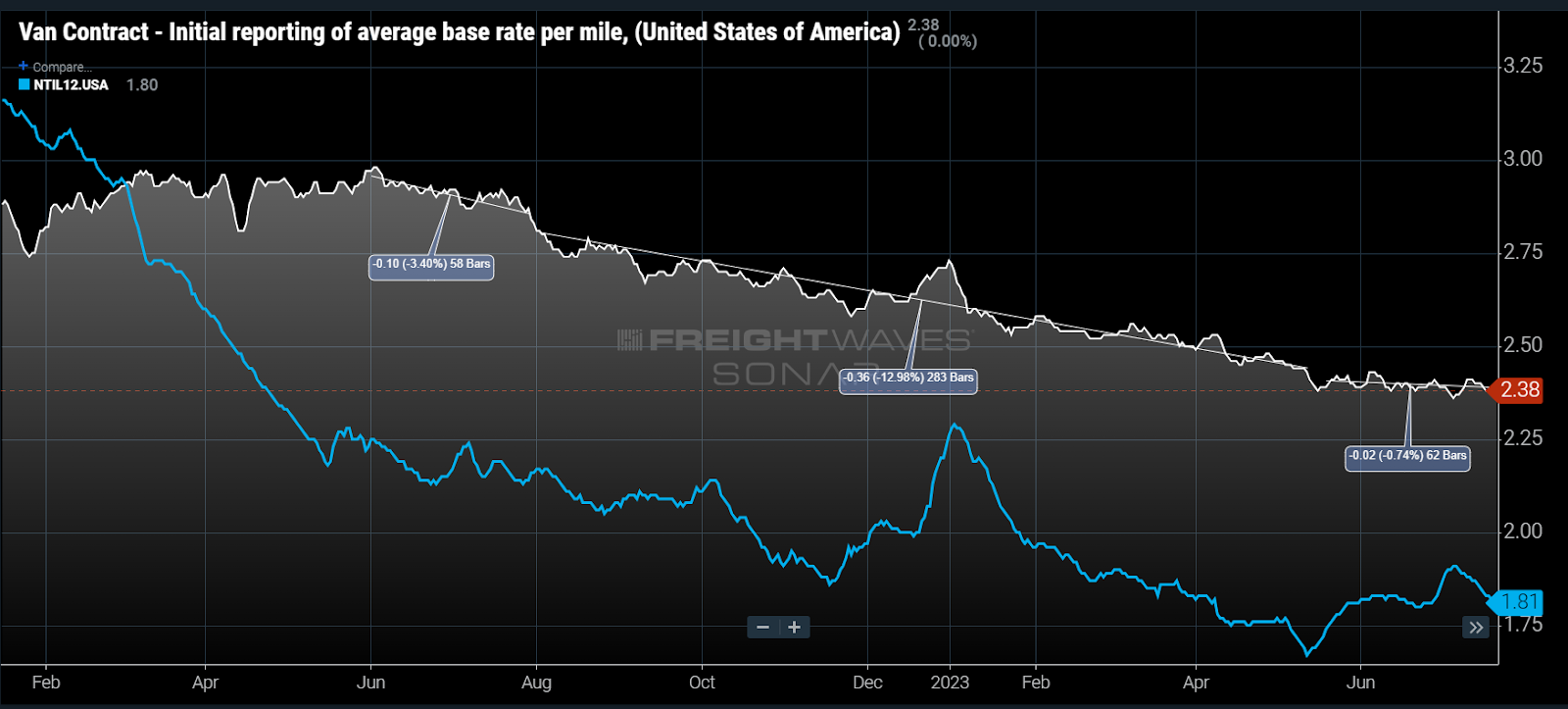

Chart of the Week: Van Contract Initial reporting of average base rate per mile, National Truckload Index excluding estimated fuel costs above $1.20/gal – USA SONAR: VCRPM1.USA, NTIL12.USA

Truckload dry van contract rates (VCRPM1) have flatlined over the past two months after dropping ~13% over the previous nine months. This is occurring despite spot rates (NTIL12) still offering a 20% discount on average. Why is that this happening?

Out of season

Traditional “bid season,” during which the majority of the shippers send out RFPs for transportation providers to submit prices for his or her services for what is often a yr, occurs Q4 into Q1 of the next yr. Implementation of the brand new rates tends to occur in Q1-Q2.

Which means that contract rates typically stabilize through the center of the yr. For the period during and following the pandemic, contract rates haven’t had many periods of stability as a result of the large amount of volatility in demand making a rapidly changing transportation market.

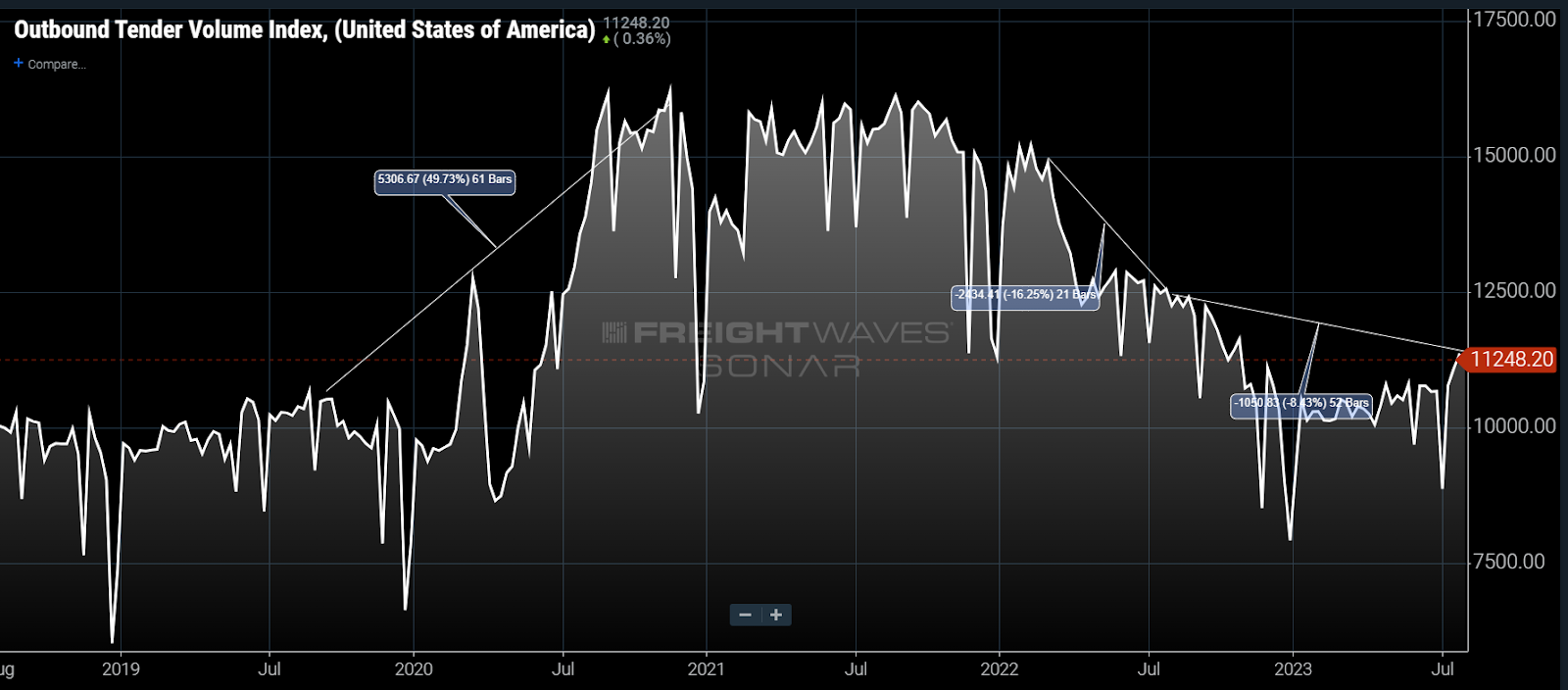

The national Outbound Tender Volume Index (OTVI), which measures shipper requests for contracted capability, jumped ~50% from July 2019 to July 2020. The majority of that jump got here from April to July 2020. The OTVI fell 30% throughout 2022 because the pandemic-era consumption boom ended. Volume has been relatively stable as compared through most of 2023.

Principally, the market has flipped from an excessive amount of capability to way too little and now way an excessive amount of over the past 4 years. This has also disrupted the traditional cadence of bidding.

Less negotiation

Many firms used mini-bids or put special project bids out available on the market for carriers to bid for shorter periods of time just to make sure higher levels of service while capability was tight. Once demand collapsed, some transportation providers offered early rate reductions prior to the bid to lock in rates and avoid exposure to the majority of the market downturn.

Brokerages have leaned into their ability to be nimble and renegotiate because the capability is in oversupply, making the most of their edge in a transitional market. Last summer, rates fell 4% from June to August. The present data shows this renegotiation cadence could also be slowing.

Spot market stability

While spot rates excluding fuel costs above $1.20 per gallon (to make it comparable to a typical fuel surcharge) are still averaging a 23% discount to the contract market, they’re up roughly 4% off their spring average. Pair this increase with a jump in demand and there might be some market-level pressure arising from shippers being busier than expected, keeping them from reevaluating their current costs prior to their seasonal offering.

The bid process could be very labor intensive and takes months for the most important shippers to organize and execute. Shippers are getting the service they need with budgets also greater than likely being in a very good position as they were set on some level of pandemic-era cost assumptions.

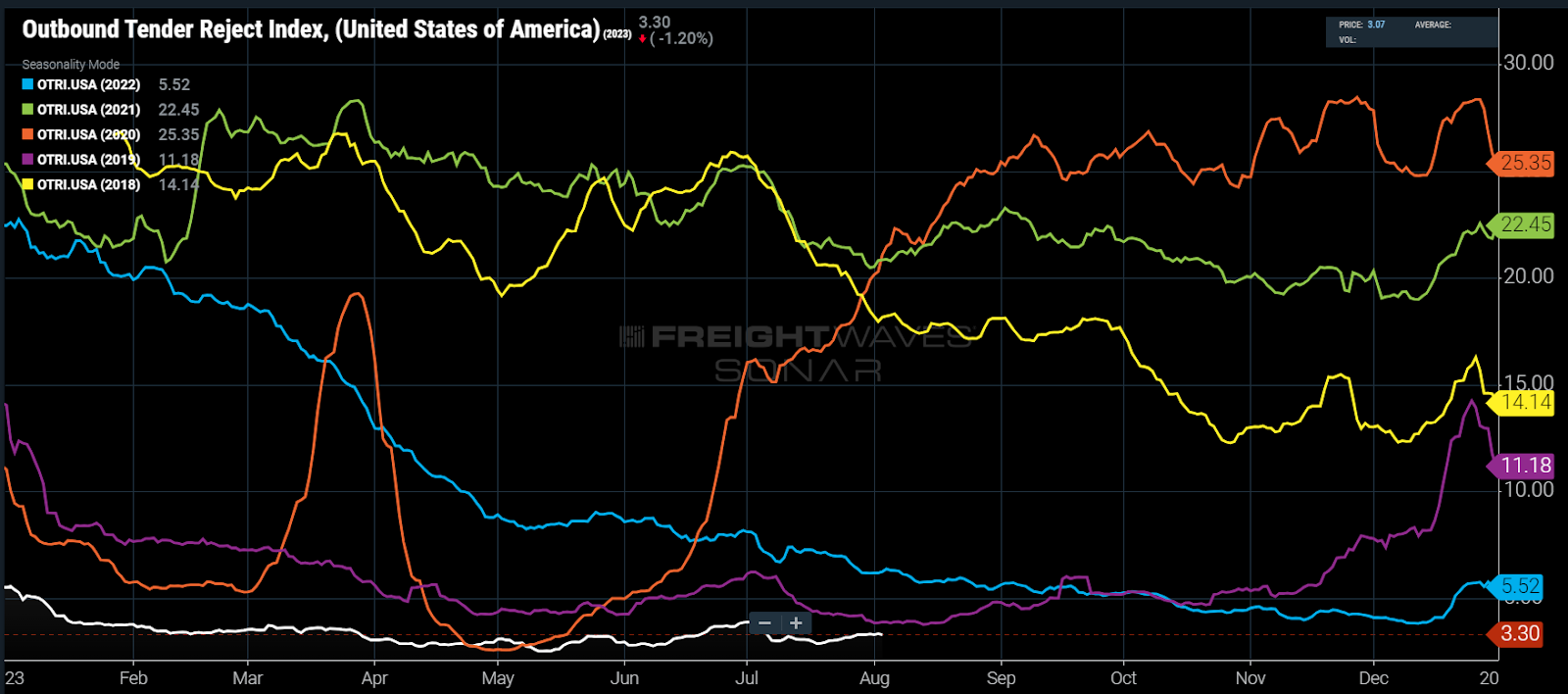

Tender rejection rates are still hovering around all-time lows for the summer. Unfortunately for transportation providers, this also means they’ll have to take care of an aggressive posture when competing for business throughout the upcoming bid season.

Service or price

Anecdotally, many firms have stated they’re focused more on constructing a stable relationship with their transportation provider partners with a commitment to service. This is smart since consistent service saves far more money in the long term, though it’s difficult to quantify when making an annual budget — especially when capability is ample.

Firms will definitely be seeking to get probably the most bang for his or her buck this upcoming bid season, but transportation managers are more aware than ever that market conditions can change rapidly and this environment of abundant capability shouldn’t be sustainable. This idea is difficult to sell to people outside of transportation (their bosses), meaning rates usually tend to resume at a faster pace of decline — which can only make them less reliable in the long run.

In regards to the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from 1000’s of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, survive the front page. After that, the Chart of the Week can be archived on FreightWaves.com for future reference.

SONAR aggregates data from a whole lot of sources, presenting the information in charts and maps and providing commentary on what freight market experts need to know concerning the industry in real time.

The FreightWaves data science and product teams are releasing recent datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post Contract rate decline takes pause despite significant spot market discount appeared first on FreightWaves.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/TCIQQJM5RRHSJMHIWL7VR2L3BI.jpg)