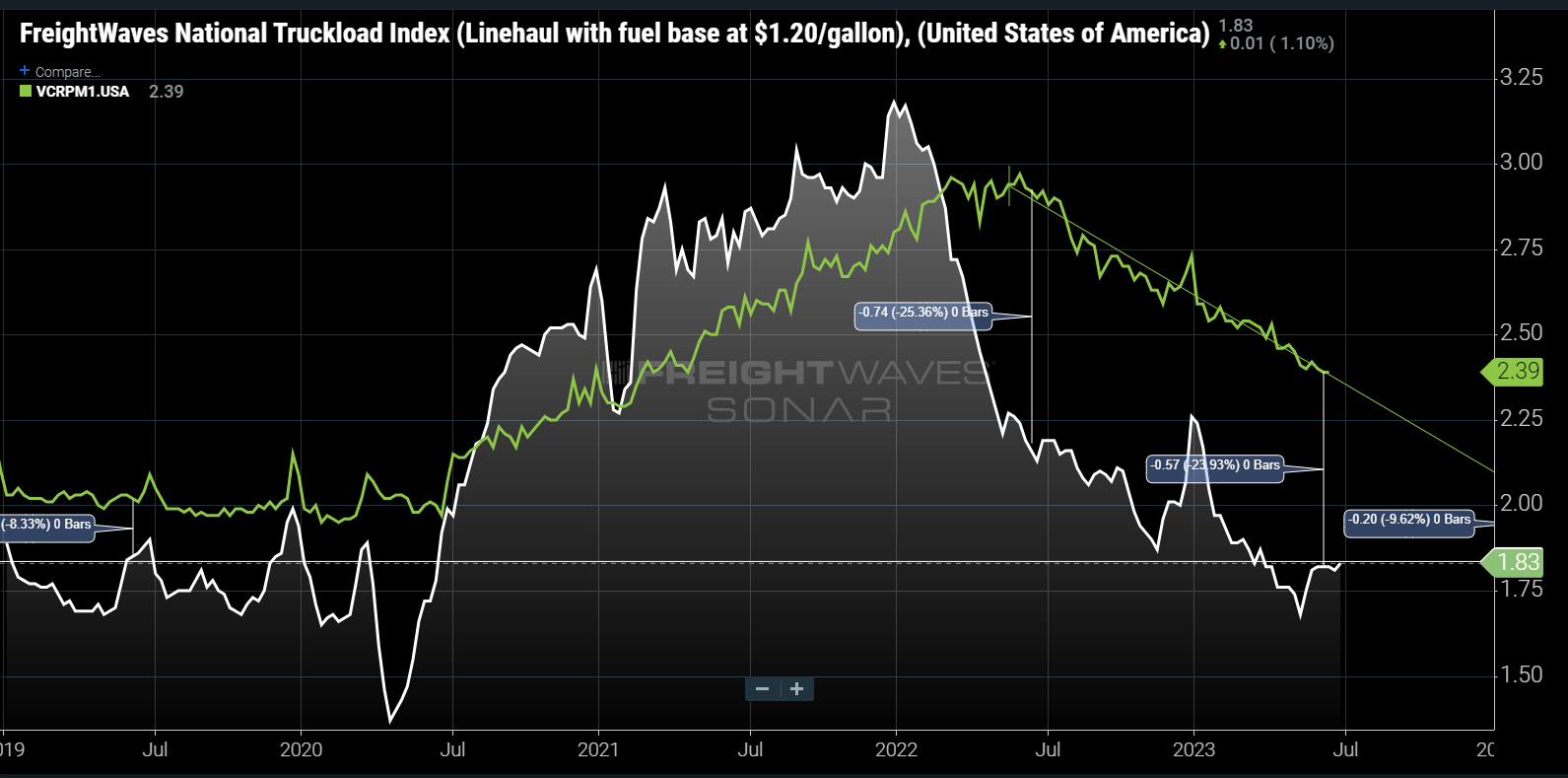

Chart of the Week: National Truckload Index Linehaul Only, Outbound Tender Rejection Index – USA SONAR: NTIL12.USA, VCRPM1.USA

The connection between dry van truckload contract (VCRPM1) and spot (NTIL12) rates stays nearly unchanged in comparison with last June, as each have fallen at nearly the identical pace over the past 12 months.

Spot rates appear to have hit a floor this summer, suggesting carriers have hit their park or drive threshold on the transactional marketplace for now with contract rates continuing to drop. If the spread between these two figures narrows — at the same time as demand falls — capability will develop into increasingly inconsistent to secure.

The domestic truckload market has been in freefall since last March with spot rates reacting first and the slower contracts — typically negotiated on three- to 12-month terms — starting a slow slide in late summer. The explanation is easy: Demand fell off a cliff after shippers stopped their “just-in-case” over-ordering strategy brought on by an unreliable supply chain environment through the pandemic.

The top result’s after nearly two years of overheated and unsustainable demand growth, capability has also increased significantly. The issue now could be that demand has retreated almost entirely to where it was in 2019, leaving many trucks with nothing to maneuver and a spot market filled with desperation.

It’s a buyer’s market

In June of 2019 the spot rate excluding fuel costs above $1.20 per gallon — comparable to a contract rate less a typical fuel surcharge — was offering about an 8% discount. The 2019 market was also fairly loose with abundant capability. Currently the spot market is moving at a ~23% discount.

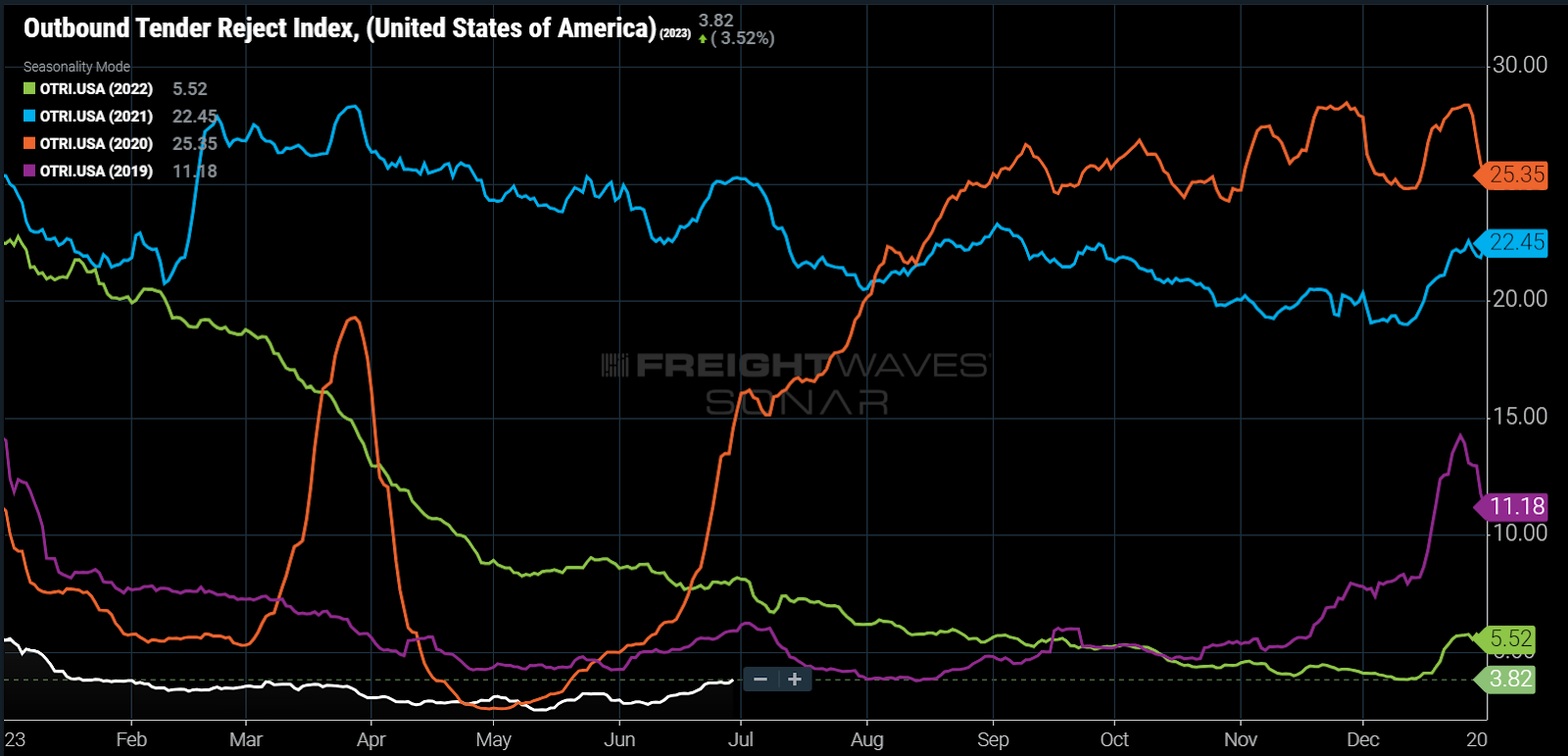

The national Outbound Tender Reject Index (OTRI) measures the speed that carriers reject contract load coverage requests from their customers. The pandemic years of 2020-21 averaged above 20% — 1 in 5 loads rejected — while 2019 averaged around 6% — 1 in ~16. The typical OTRI value to date in 2023 is 3.5% — 1 in 28.

With spot rates moving at such a powerful historical discount, carriers are incented to cover every part they’ll under the more lucrative contract rates — keeping OTRI low. An OTRI value below 5% is indicative of a market through which carriers are in strong competition for business, pushing contract rates lower.

Mix the low rejection rate with the spot market discount and this implies contract rates still have an extended strategy to fall unless capability exits the market significantly or demand spikes.

How briskly will rates fall?

For this forecasting exercise let’s assume spot rates is not going to fall significantly over the subsequent six months, but they are going to likely spike around Christmas as they did this past yr, despite the soft environment.

Contract rates have fallen in nearly an ideal linear regression over the past yr, so applying the identical trend will not be a dangerous assumption. There may be an argument to be made that some acceleration in decline is due, because of the incontrovertible fact that many shippers’ transportation budgets will take a success in the subsequent yr and most of the current rates were put in place before anyone realized the market had turned.

Assuming a flat spot rate trend and continuing the present rate of decline for contracts, the spread will drop below 10% around the vacation season. This might make for a rude awakening for a lot of shippers which have had an prolonged period of easy sourcing.

As carriers see spot load offerings improve in relation to their contract freight, they will likely be tempted to divert capability to cover potentially more lucrative offerings, especially considering a lot of them have been struggling for over a yr.

Spot rates are likely to jump around Thanksgiving and Christmas as retailers recognize what goods are most in demand. Firms are willing to spend more on transportation to make sure sales usually are not hindered by lack of inventory. The smaller window of opportunity also means increased service expectations — one other inflationary force.

While this will not be expected to be anywhere near the disruption in 2020-21, it could catch a couple of corporations off guard during a critical time frame in a slowing goods economy. Many retail corporations were capable of mask the provision chain issues through the pandemic resulting from sales growth. With demand in decline, inventory shortfalls will possibly hurt more in 2023 than they did then.

Concerning the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from 1000’s of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, live to tell the tale the front page. After that, the Chart of the Week will likely be archived on FreightWaves.com for future reference.

SONAR aggregates data from a whole bunch of sources, presenting the information in charts and maps and providing commentary on what freight market experts need to know in regards to the industry in real time.

The FreightWaves data science and product teams are releasing latest datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

{kind=link}