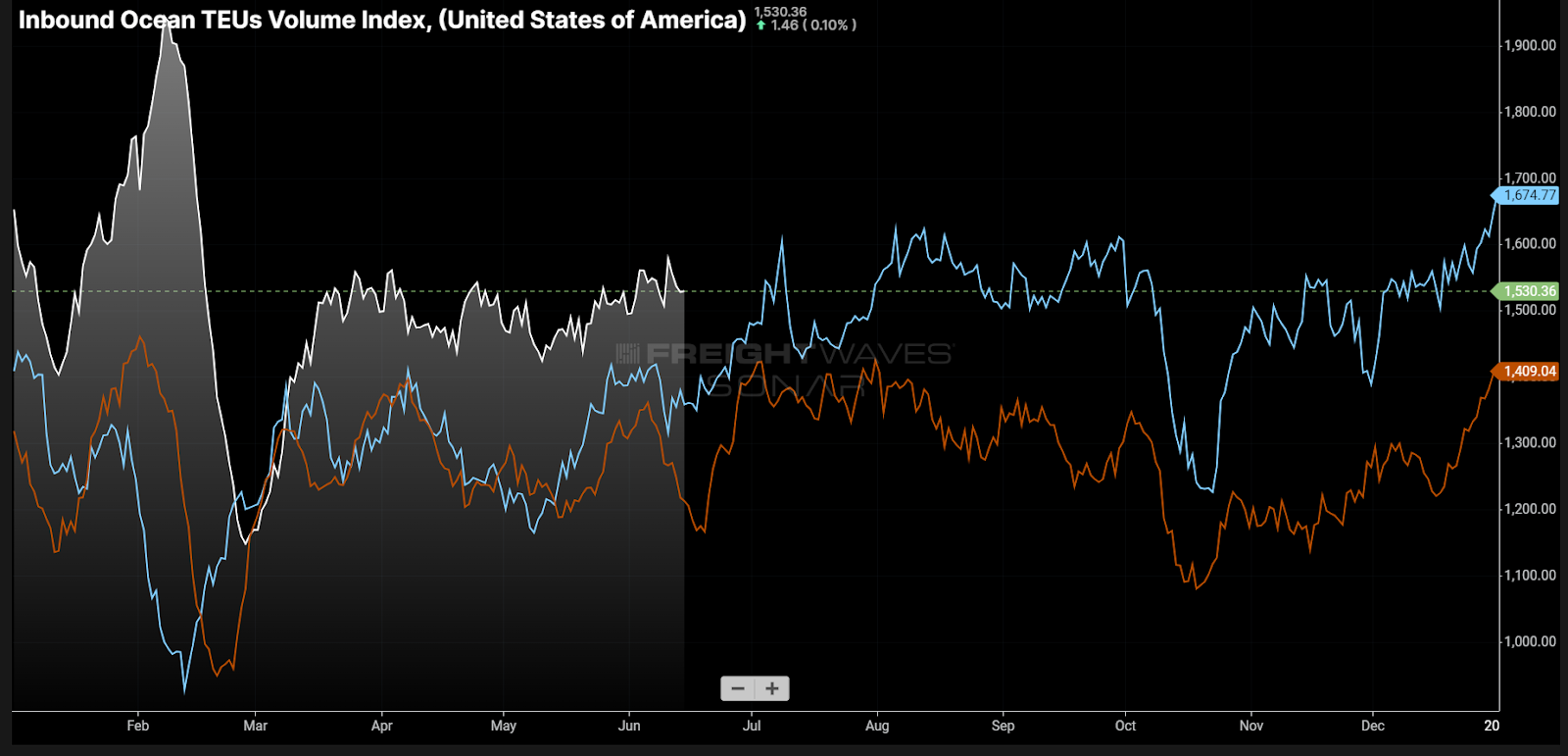

Chart of the Week: Inbound Ocean TEUs Index – USA SONAR: IOTI.USA

Bookings for 20-foot equivalent container imports (IOTI) are up 27% versus mid-June of 2019 and 11% over last yr. With all of the talk and expectations of nearshoring, goods coming from overseas are still flowing strong and having a noticeable impact on domestic transportation patterns.

The IOTI is a 14-day moving average index of orders (bookings) of 20-foot equivalent containers (TEU) based on the time of departure from the port of origin. Bookings lead customs clearings by about two to 3 weeks on goods coming from China to Los Angeles, and over a month on containers landing on the East Coast.

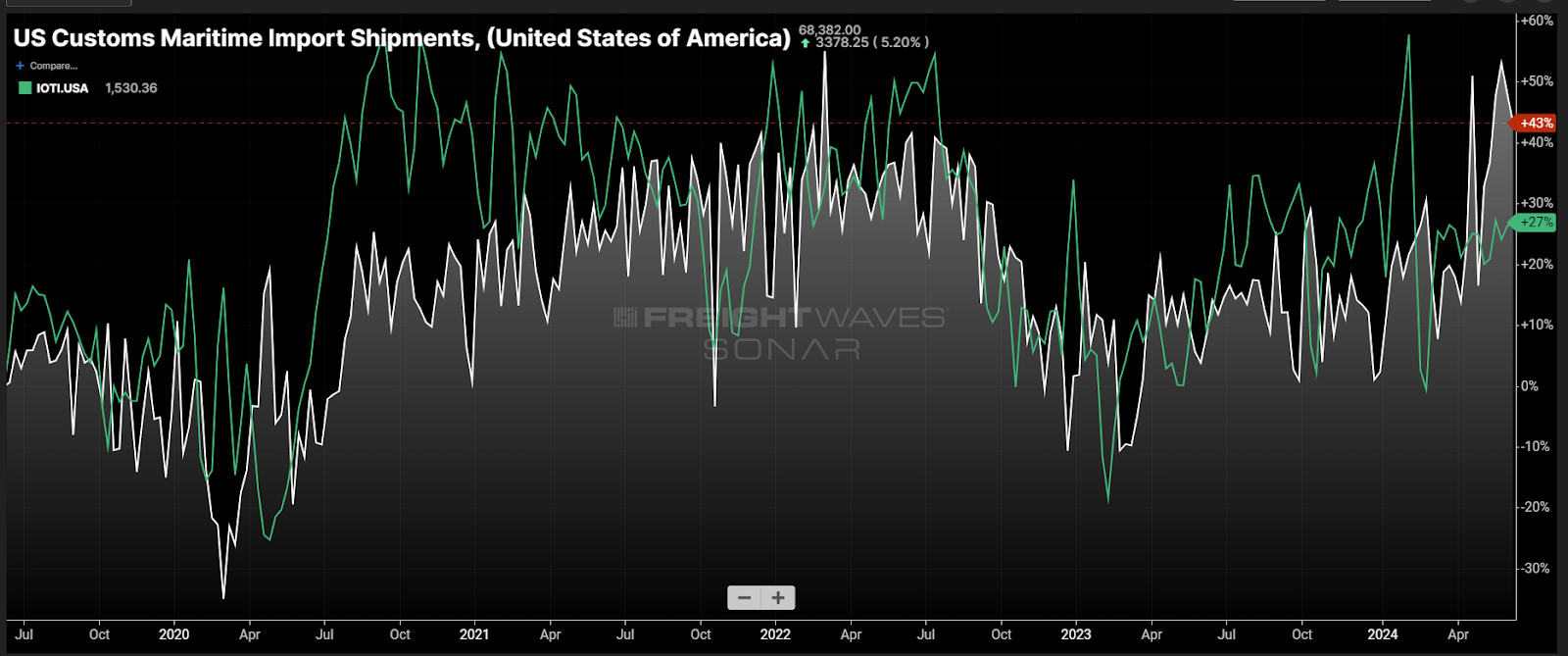

Customs and the IOTI have a good correlation on a lag, but customs is inhibited by port infrastructure and labor, while bookings have little to no limitation on scale. Customs clearings within the above chart are based on shipments and never containers, however the connection remains to be present.

The geopolitical environment is arguably more chaotic than it was in 2019, and the decision for supply chains to diversify away from riskier sources of materials and production has been growing throughout the pandemic era and beyond. The world has entered a phase of deglobalization—a minimum of within the headlines.

The maritime import data paints a really different picture, but really doesn’t disagree with the premise that the world climate is more challenged than it was five years ago.

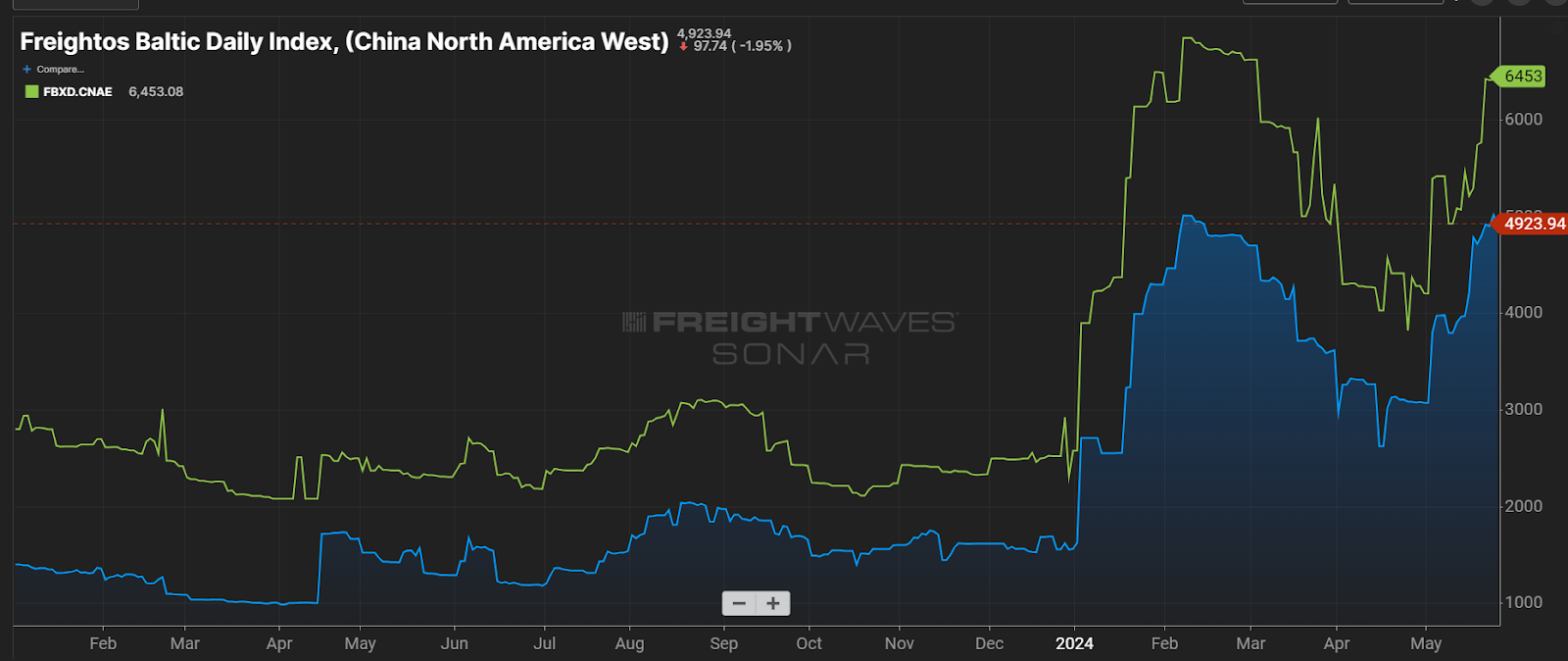

One among the explanations for import growth comes from the concerns over container-ship capability being tied up in longer transits as they fight to avoid the conflict within the Middle East. While it doesn’t have a powerful direct influence on North American import lanes from Asia—where many of the imports originate—it does impact global capability as a complete. More capability is required on Asia to Europe lanes, potentially dragging eastbound ships.

Spot rates on 40-foot equivalent units (FEU) jumped to start out the yr on the heels of the growing conflict across the Suez Canal and the Lunar Recent 12 months demand before slowly sliding. Those rates have jumped once more, remaining well above pre-pandemic norms.

There have been claims of carriers managing capability availability, because the variety of boats has been growing steadily for the past few years and, in theory, should find a way to handle the extra demand and not using a 50% increase in rates over the course of a month.

Whatever the carrier’s ability or reason, shippers find themselves once more coping with uncertainty in rates and services on goods coming from across the ocean. This may increasingly be causing firms to drag forward orders with longer lead times to expected success.

Taking a look at the IOTI, there was a noticeable absence of a seasonal downward slide in April that was present each in 2019 and last yr. Each years’ IOTI values fell 15% from early April to mid-May, whereas this yr there was only a moderate downward trend of perhaps a 5% deterioration.

Import bookings are up significantly to the most important U.S. port complexes versus where they were five years ago. Peak season for import demand is often July and August, which implies considered one of two things is feasible.

Peak import season shall be muted because firms have been more proactive or the doors are about to get blown off the ports. That is actually saying we’re back in a particularly uncertain environment that we thought we had left behind us.

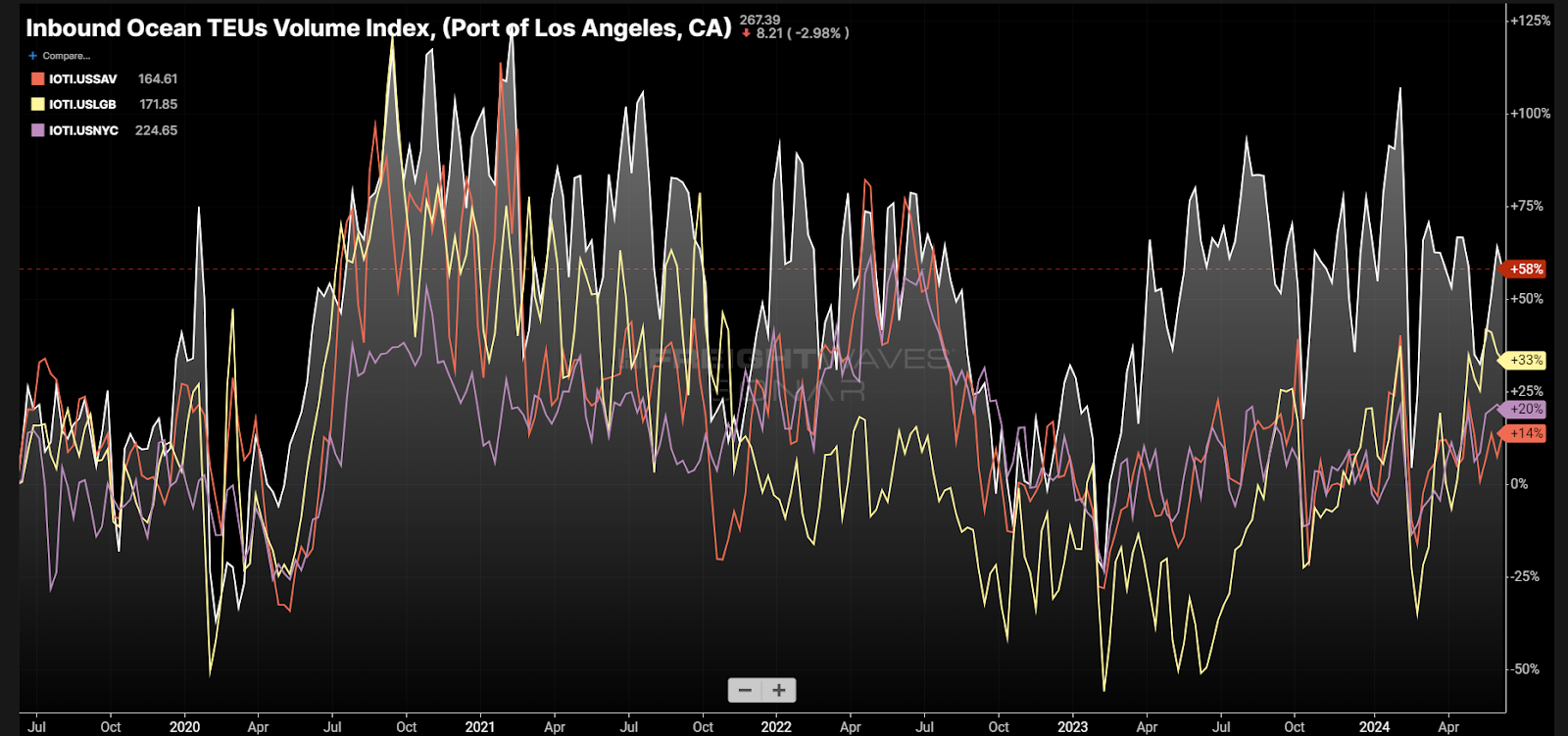

Domestic transportation has also been affected. International container volumes (20- and 40-foot containers primarily used for maritime shipping) moving on the rails are up 16% yr over yr. Los Angeles’ outbound truckload tender volumes are up 35%, helping push tender rejection rates to their highest levels since 2022. Spot rates from Los Angeles to Chicago have increased 7% over the past month and 21% since March, in keeping with FreightWaves TRAC.

In regards to the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that gives an interesting data point to explain the state of the freight markets. A chart is chosen from hundreds of potential charts on SONAR to assist participants visualize the freight market in real time. Each week a Market Expert will post a chart, together with commentary, survive the front page. After that, the Chart of the Week shall be archived on FreightWaves.com for future reference.

SONAR aggregates data from a whole bunch of sources, presenting the information in charts and maps and providing commentary on what freight market experts need to know in regards to the industry in real time.

The FreightWaves data science and product teams are releasing recent datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

The post What nearshoring? appeared first on FreightWaves.

:quality(70)/cloudfront-us-east-1.images.arcpublishing.com/archetype/PASJG3E2ZZACLF5R5ZZ2EOAKNI.jpg)